DRAFT- PRE-DECISIONAL / CONFIDENTIAL / NOT FOR DISTRIBUTION

Coronavirus State and Local Fiscal Recovery Fund:

i DRAFT- PRE-DECISIONAL / CONFIDENTIAL / NOT FOR DISTRIBUTION

User Guide: Treasury’s Portal for Recipient Reporting

August 9, 2021

Version: 1.0

XXX

Version: 1.0

January XX, 2022

Version 1

January 24, 2022

Version: 1.1

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide i

Table of Contents

Section I. Reporting Basics ................................................................................................. 1

Section II. Navigation and Logistics .................................................................................... 3

Section III. Reporting Requirements .................................................................................... 8

Section IV. Project and Expenditure Report ....................................................................... 12

Appendix A – Designating SLFRF Points of Contact by SLFRF Account Administrators 42

Appendix B – Bulk File Upload Overview ............................................................................... 49

Appendix C – Expenditure Categories and Template Mapping ............................................ 65

Appendix D – SLFRF Expenditure Category Programmatic Data and Other Information . 68

Appendix E – List of Sectors ................................................................................................... 78

Appendix F – Frequently Asked Questions ............................................................................ 79

List of Figures

Figure 1 Landing Page .................................................................................................................. 3

Figure 2 Navigation Bar ................................................................................................................ 4

Figure 3 Sample Bulk Upload Icon ............................................................................................... 5

Figure 4 Successful Bulk Upload Example ................................................................................... 5

Figure 5 Bulk Upload Validation Screen ....................................................................................... 6

Figure 6 Manual Validation Text Box ............................................................................................ 6

Figure 7 Sidebar indicating Unsubmit Button ................................................................................ 7

Figure 8 Relationship between Expenditure Categories and Multiple Projects .......................... 11

Figure 9 Recipient Information .................................................................................................... 12

Figure 10 Point of Contact List .................................................................................................... 13

Figure 11 Budget Approval and Obligation ................................................................................. 13

Figure 12 SAM.gov question ....................................................................................................... 14

Figure 13 Additional SAM.gov questions (1) ............................................................................... 14

Figure 14 Additional Sam.gov questions (2) ............................................................................... 14

Figure 15 Record of Highest Paid Officer ................................................................................... 15

Figure 16 No Projects Available Option ...................................................................................... 16

Figure 17 No Projects Available Entry Screen ............................................................................ 16

Figure 18 My Projects Screen Example ...................................................................................... 18

Figure 19 Project Expenditure Category Group .......................................................................... 18

Figure 20 Project Expenditure Category ..................................................................................... 19

Figure 21 Bulk Upload for EC 1.1 ............................................................................................... 19

Figure 22 Project Entry Screen ................................................................................................... 20

Figure 23 Manual Entry for EC 1.9 ............................................................................................. 21

Figure 24 Programmatic Data for EC 1.9 .................................................................................... 21

Figure 25 Edit and Delete Project Screen ................................................................................... 22

Figure 26 Premium Pay Screen and Additional Questions ......................................................... 23

Figure 27 Programmatic Data for Infrastructure Projects ........................................................... 25

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide ii

Figure 28 Davis Bacon Certification ............................................................................................ 26

Figure 29 Additional Questions if Response to Davis Bacon Certification is "No" ...................... 26

Figure 30 Certification for Labor Agreements ............................................................................. 27

Figure 31 Additional Questions if response is "No"..................................................................... 27

Figure 32 Revenue Replacement Screen ................................................................................... 29

Figure 33 Subrecipient Bulk Upload Icon .................................................................................... 31

Figure 34 Manually Create a Subrecipient or Beneficiary ........................................................... 31

Figure 35 Sam.gov Questions for Subrecipients ........................................................................ 32

Figure 36 Additional SAM.gov questions for Subrecipients ........................................................ 32

Figure 37 Five Highest Paid Officers for Subrecipients or Beneficiaries..................................... 33

Figure 38 Subrecipients Entered ................................................................................................ 33

Figure 39 Subaward Bulk Upload (1) .......................................................................................... 34

Figure 40 Subaward Bulk Upload (2) .......................................................................................... 34

Figure 41 Subaward Reporting ................................................................................................... 35

Figure 42 Subaward Entered ...................................................................................................... 35

Figure 43 Expenditures >$50,000 ............................................................................................... 37

Figure 44 Aggregated Expenditures <$50,000 ........................................................................... 37

Figure 45 Payments to Individuals .............................................................................................. 38

Figure 46 Tax Offset Provision Screen ....................................................................................... 39

Figure 47 Official Certification ..................................................................................................... 39

Figure 48 Summary of Reported Information .............................................................................. 40

Figure 49 Submission Verification .............................................................................................. 40

Figure 50 Submission Verification with additional language ....................................................... 41

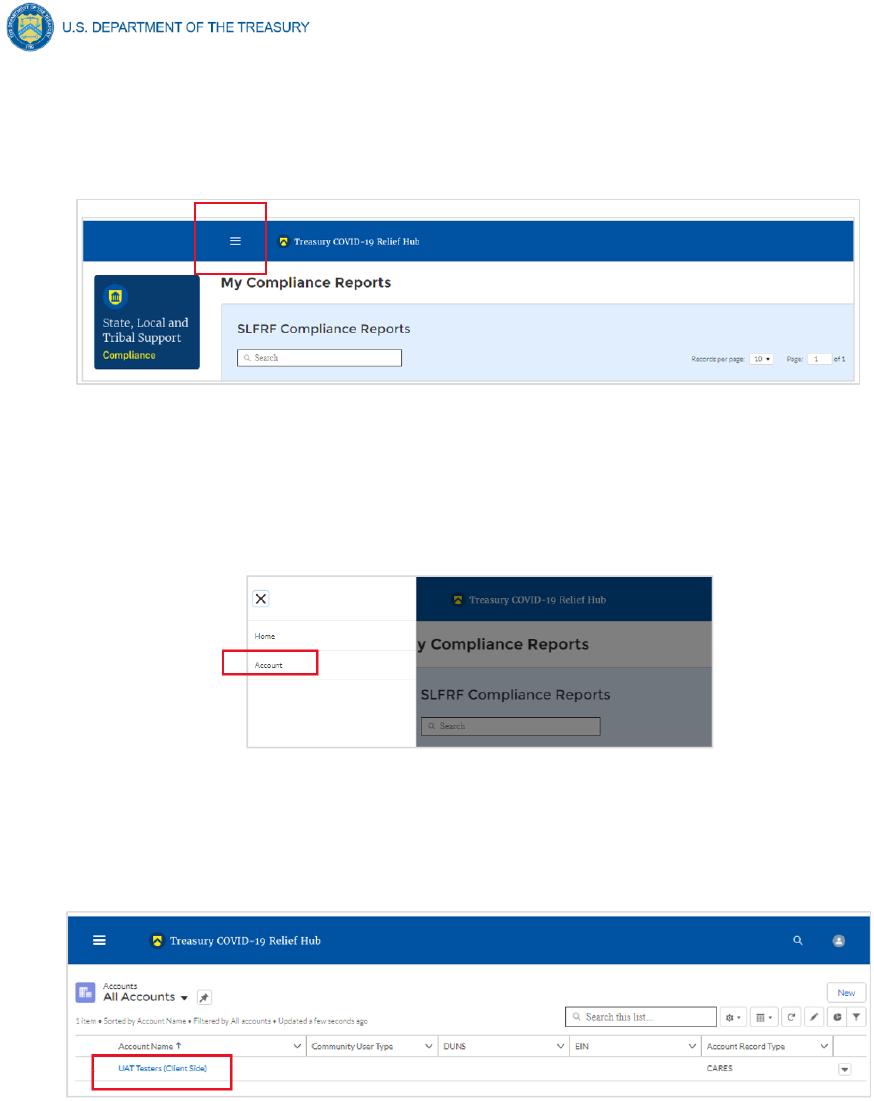

Figure 51 State, Local and Tribal Support Landing Page ........................................................... 42

Figure 52 My Compliance Reports ............................................................................................. 43

Figure 53 Account ....................................................................................................................... 43

Figure 54 Account Name ............................................................................................................ 43

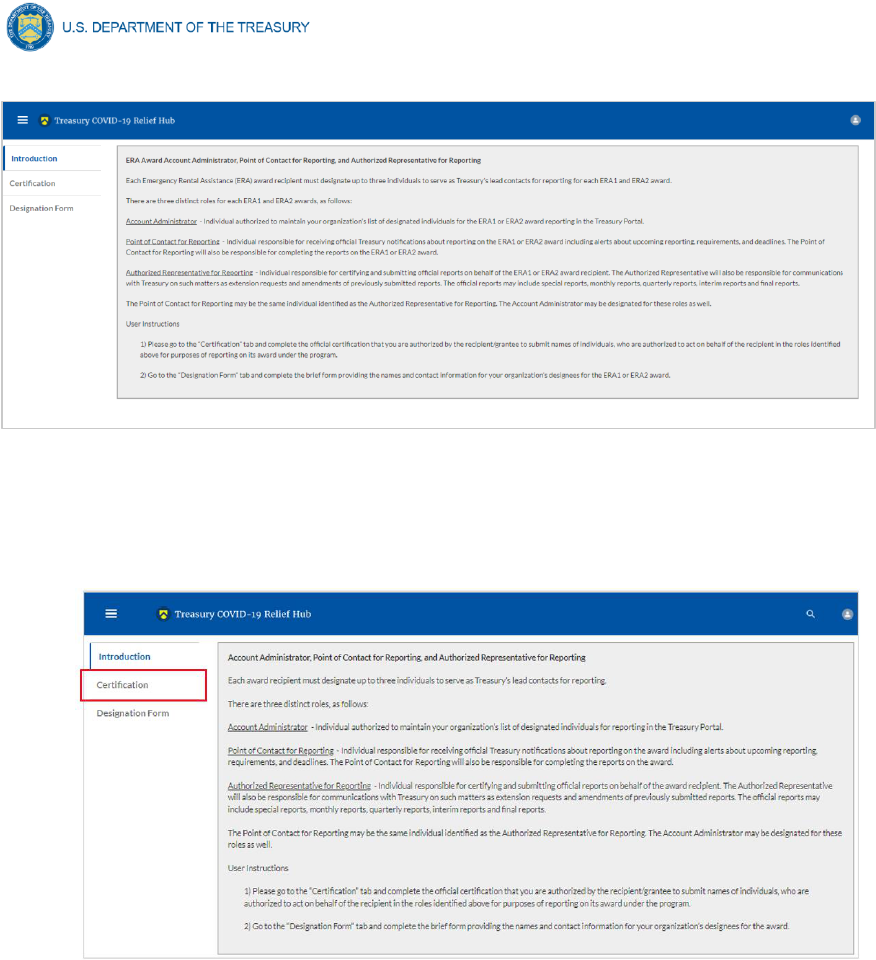

Figure 55 Landing Page .............................................................................................................. 44

Figure 56 Certification ................................................................................................................. 44

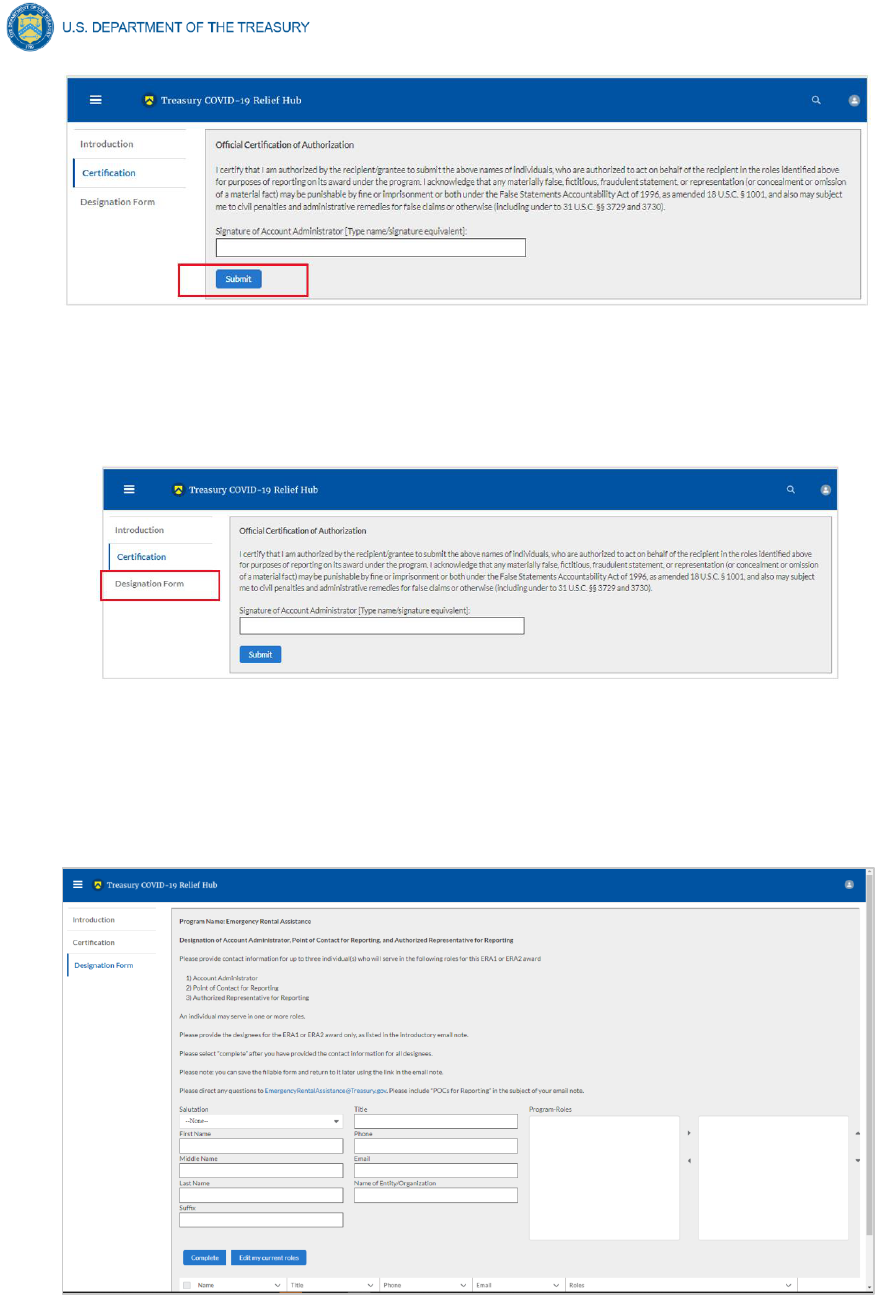

Figure 57 Official Certification of Authorization ........................................................................... 45

Figure 58 Designation Form ....................................................................................................... 45

Figure 59 Designation of Account Administrator, Point of Contact of Reporting and Authorized

Representative for Reporting ...................................................................................................... 45

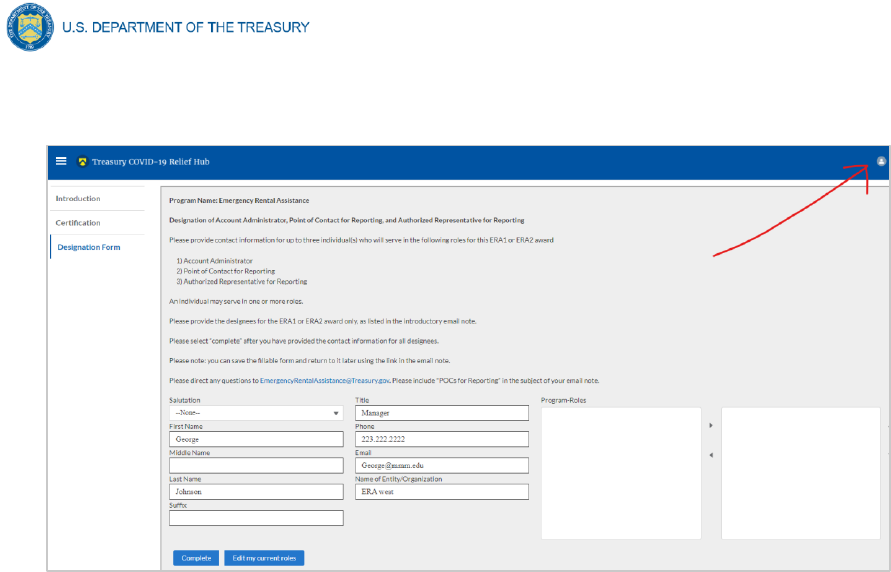

Figure 60 Designation Form ....................................................................................................... 47

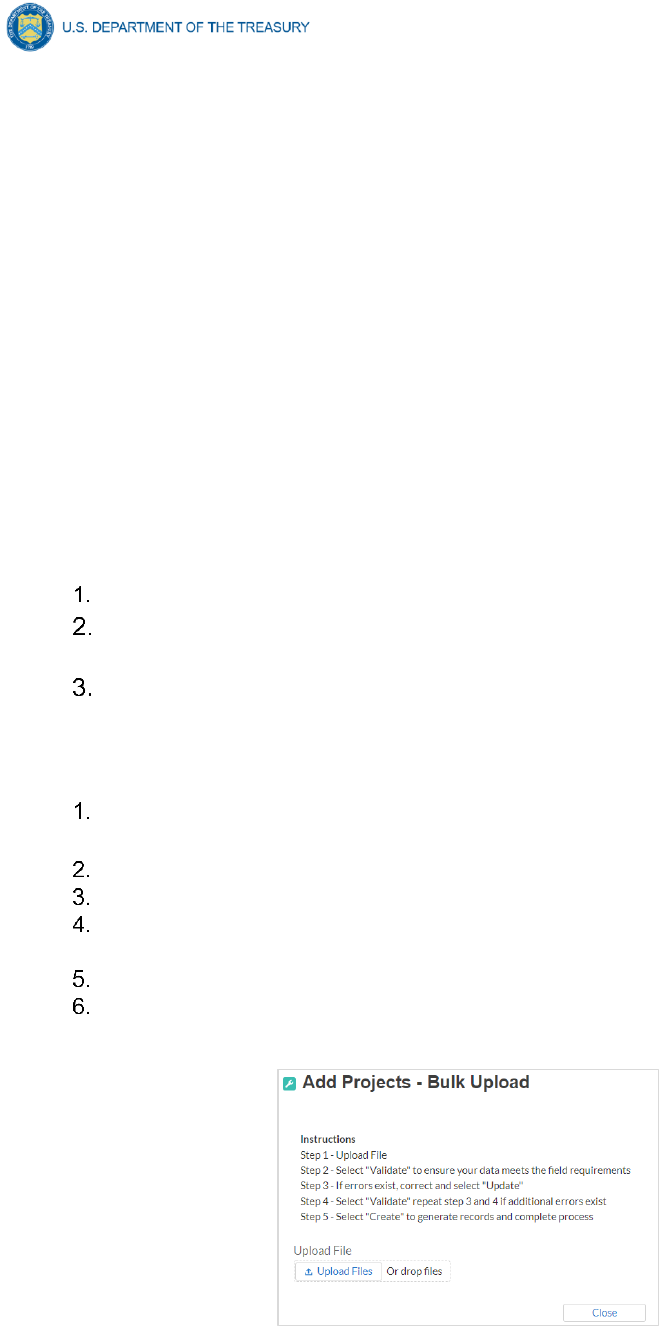

Figure 61 Bulk Upload pop up .................................................................................................... 50

Figure 62 File uploaded message ............................................................................................... 51

Figure 63 File added to Bulk Upload portal ................................................................................. 51

Figure 64 Listing of Bulk Upload Errors ...................................................................................... 51

Figure 65 Bulk Upload Creation .................................................................................................. 52

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 1

Section I. Reporting Basics

a) Overview

This document provides information on using Treasury’s Portal to submit the required

Coronavirus State and Local Fiscal Recovery Funds (SLFRF) Project and Expenditure (P&E)

reports. It is a supplement to the Compliance and Reporting Guidance (Reporting Guidance),

which contains relevant information and guidance on the reporting requirements.

Additionally, you should visit Treasury’s SLFRF home page for the latest guidance and updates

on programmatic and reporting topics, as well as information on Treasury’s Interim Final Rule

(IFR).

Each SLFRF recipient is required to submit periodic reports with current performance and

financial information including background information about the SLFRF projects that are the

subjects of the reports; and financial information with details about obligations, expenditures,

direct payments, and subawards.

b) What is Covered in this User Guide?

This User Guide contains detailed guidance and instructions for SLFRF recipients in using

Treasury’s Portal for submitting the Project and Expenditure reports. All recipients must submit

the required reports via Treasury’s Portal. This guide is not comprehensive and is meant to be

used in conjunction with the documents mentioned above.

This User Guide provides detailed instructions to help recipients enter and submit the following:

• Project data

• Subrecipient data

• Subaward data

• Expenditure data

• Project and Expenditure Bulk Upload Templates

c) Designating Staff for Key Roles in Managing SLFRF Reports User Designations

SLFRF recipients are required to designate staff or officials for the following three roles in

managing reports for their SLFRF award. Recipients must make the required designations prior

to accessing Treasury’s Portal. The required roles are as follows:

• Account Administrator for the SLFRF award has the administrative role of maintaining the

names and contact information of the designated individuals for SLFRF reporting. The

Account Administrator is also responsible for working within your organization to determine

its designees for the roles of Point of Contact for Reporting and Authorized Representative

for Reporting and providing their names and contact information via Treasury’s Portal.

Finally, the Account Administrator is responsible for making any changes or updates to the

user roles as needed over the award period. We recommend that the Account Administrator

identify an individual to serve in his/her place in the event of staff changes.

• Point of Contact for Reporting is the primary contact for receiving official Treasury

notifications about reporting on the SLFRF award, including alerts about upcoming

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 2

reporting, requirements, and deadlines. The Point of Contact for Reporting is responsible for

completing the SLFRF reports.

• Authorized Representative for Reporting or ARR is responsible for certifying and

submitting official reports on behalf of the SLFRF recipient. Treasury will accept reports or

other official communications only when submitted by the Authorized Representative for

Reporting. The Authorized Representative for Reporting is also responsible for

communications with Treasury on such matters as extension requests and amendments of

previously submitted reports. The official reports may include special reports, quarterly or

annual reports, interim reports, and final reports.

Some key items to note:

• Each designated individual must register with ID.me or Login.gov for gaining access to

Treasury’s Portal.

• Users who have previously registered through ID.me may continue to access Treasury’s

Portal through that method. This link includes further instructions.

• If you have not previously registered with ID.me, you should register through Login.gov

following this link. The following links provide additional information:

o https://login.gov/create-an-account/

o https://login.gov/help/get-started/create-your-account/

• An individual may be designated for multiple roles. For example, the individual

designated as the Point of Contact for Reporting may also be designated as the

Authorized Representative for Reporting.

• The recipient may designate one individual for all three roles.

• Multiple individuals can be designated for each role.

• An organization may make changes and updates to the list of designation individuals

whenever needed. These changes must be processed by the Account Administrator.

Refer to Appendix A for guidance on designating individuals for the three roles.

The designated individuals’ names and contact information will be pre-populated in the

“Recipient Profile” portion of the recipient’s SLFRF reports, and recipients will be able to update

the information, if necessary.

Please contact SLFRP@treasury.gov for additional information on procedures for registering

with ID.me or Login.gov.

d) Questions?

If you have any questions about the SLFRF program’s reporting requirements, please contact

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 3

Section II. Navigation and Logistics

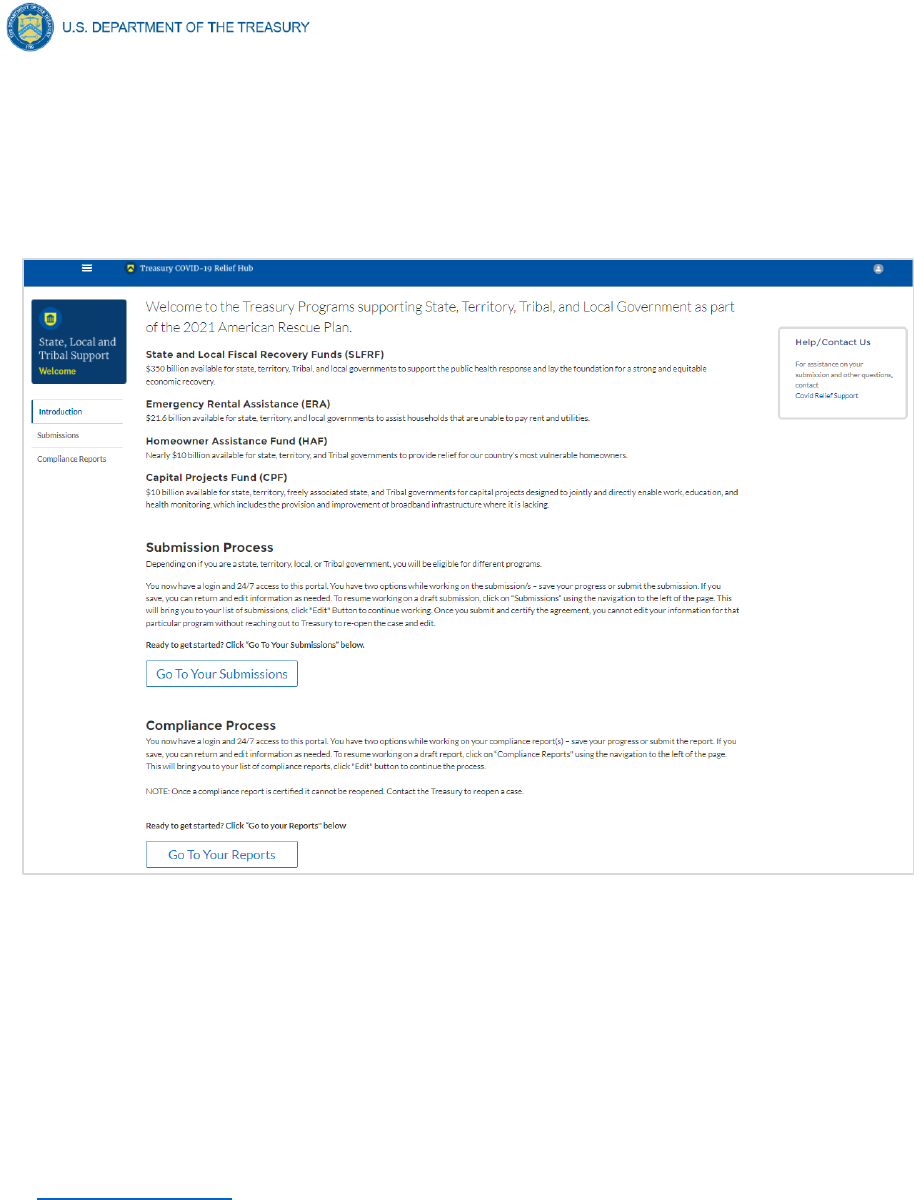

a) Login to Landing Page and Portal Navigation

After logging into Treasury’s Portal, the landing page (see Figure 1) will appear listing the

Treasury’s Office of Recovery Programs (ORP)-administered program for which your organization

may be eligible.

Figure 1 Landing Page

From the landing page, select Go to Your Reports or Compliance Reports on the left side panel

to be taken to a list of options for the programs you have access to under the Report Selection

section.

At this time, you may select the Project and Expenditures report.

Each listed report constitutes a link to that specific report’s online forms. Selecting a report from

the landing page will open the first in a series of screens.

To begin completing a specific report, click on Provide Information for the given report. Refer to

the Reporting Guidance for details about each type of required report for submittal.

The Navigation Bar (see Figure 2) on the left of Treasury’s Portal will allow you to freely move

between screens.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 4

Figure 2 Navigation Bar

b) Helpful Tips/Shortcuts for Submitting Data to Treasury’s Portal

Treasury’s Portal leads you through a series of online forms that, when completed, will fulfill

your reporting obligations. While navigating through Treasury’s Portal and submitting required

information, users will have the option of manually entering data directly into Treasury’s Portal

or providing information via a bulk upload file that includes all relevant information in a Treasury

approved process and format.

Bulk File Upload Files

Recipients can use the bulk upload function for providing required information for the modules

listed here:

• Project Overview

• Subrecipients

• Subawards

• Expenditures

When using the bulk upload, recipients must provide the required information in specified

formats and use the Treasury approved templates for each respective bulk upload. Recipients

must download each of the templates separately from within the relevant Treasury’s Portal

module.

Please see Appendix B – Bulk File Upload Overview for complete guidance on using this

important function.

Modules accepting bulk upload files are clearly marked in Treasury’s Portal and identified in

later sections of this User Guide. The template for each upload file is available in the relevant

module for download (see Figure 3).

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 5

Figure 3 Sample Bulk Upload Icon

All bulk file templates download in the .xls format, but these files must be converted to .csv

format to properly upload. When you click the upload button you will be directed to an upload

screen. You can either choose to add files or drag and drop files to initiate the bulk upload

(see Figure 4). Refer to Appendix B for additional instructions to submit bulk upload file.

Figure 4 Successful Bulk Upload Example

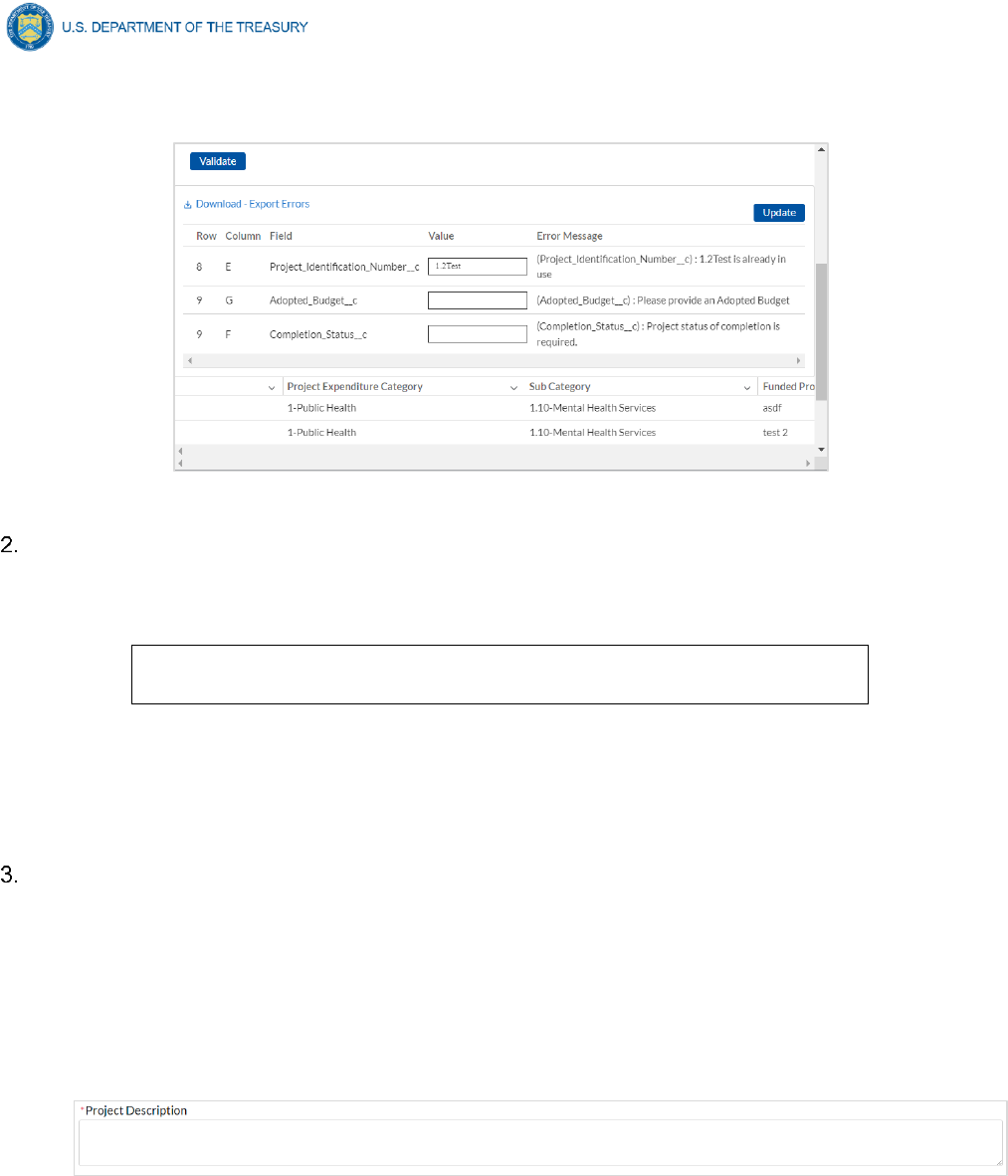

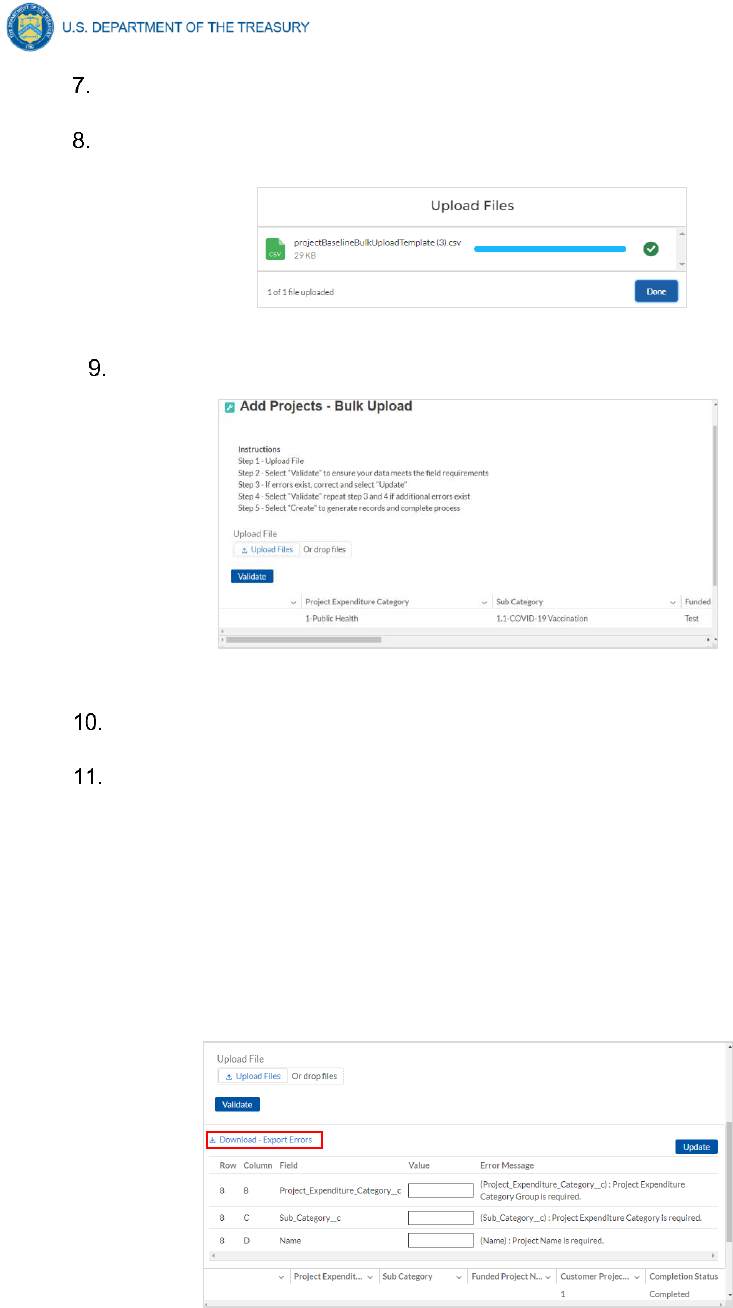

Treasury’s Portal will reject the file if an incorrect template, data format, or file format other

than .csv is used for upload (see Figure 5). Treasury’s Portal will display an error message on

screen if the bulk data upload file contains errors. If you receive an error message, you will

need to correct the errors either in the bulk upload file or on screen and re-submit the corrected

version.

There are three common Bulk File Upload errors as described below (see Figure 5):

• Blank Data: When a required field is left blank within your bulk upload file, the specific

bulk upload file row and cell number will be provided on the screen. In the example

below, the user made an error pertaining to the “Completion Status” and the error is

located in Column F, Row 9.

• Invalid Data: Invalid data includes any type of data (numeric or text) that does not

meet the requirements set forth in the Help Text within each bulk upload template. In

the example below, the user made an error pertaining to the “Adopted Budget” and

the error is located in Column G, Row 9.

• Duplicate Data: Duplicate data includes any type of data (numeric or text) that is

repeated in the same column when the Help Text within a bulk upload template

requires a unique entry. For example, unique numbers should be provided for the

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 6

project identification number. In the example below, the user made an error pertaining

to the “Project Identification Number” and the error is in Column E, Row 8.

Figure 5 Bulk Upload Validation Screen

Manual Data Entry

Manual data entry requires you to provide inputs as instructed on the screen. Manual inputs are

described in detail below for each section of this user guide.

Note: An asterisk ( * ) indicates a required field. Entry into the field is

required before you can save or proceed to the next screen.

Your inputs will be subject to validation by Treasury’s Portal to ensure that the data provided is

consistent with expected format or description (e.g., entering “one hundred” instead of 100). If a

given data entry fails a validation rule, Treasury’s Portal will display an error for you to address.

You will not be able to submit manually entered data that does not satisfy the data validation rules.

Narrative Boxes

When filling out detailed narratives, you are encouraged to type out responses in a word

processing application (such as Microsoft Word) to minimize grammatical errors, track word

count, and concisely answer all required narrative details. You can then copy and paste the final

written narratives directly into the text boxes.

The text boxes (see Figure 6) can be expanded by clicking and dragging the icon in the bottom-

right corner.

Figure 6 Manual Validation Text Box

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 7

Corrections and Resubmissions

In the event a file is uploaded, or information is entered into Treasury’s Portal, the information

will be accepted by Treasury’s Portal as a record.

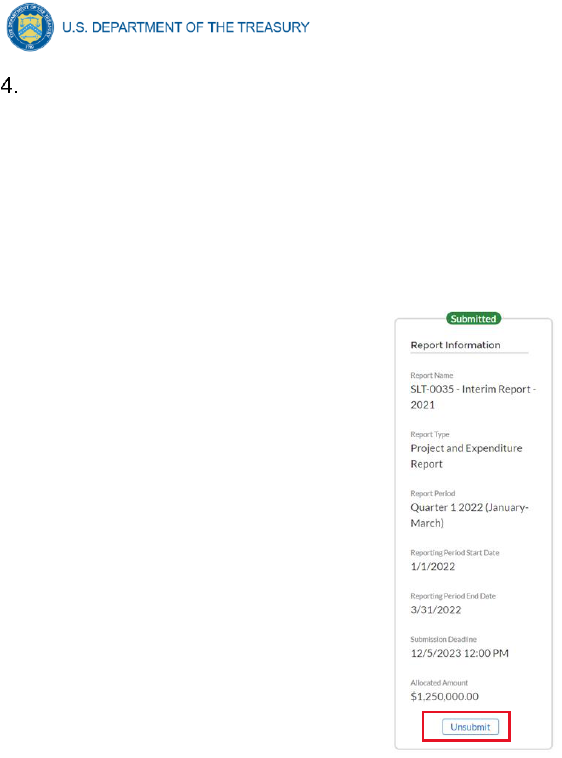

After a recipient’s submission has been certified and submitted in the system by the ARR, it can

be corrected in the Portal by selecting the Unsubmit button. Recipients may unsubmit, then

resubmit their Project and expenditure Report any time before the reporting deadline (see

Figure 7).

Figure 7 Sidebar indicating Unsubmit Button

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 8

Section III. Reporting Requirements

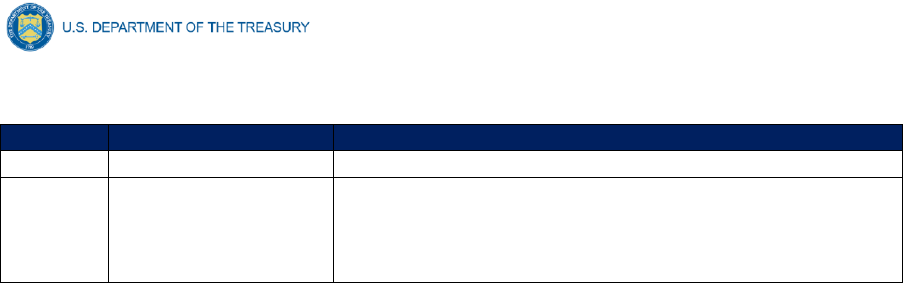

a) Reporting Requirements by Recipient

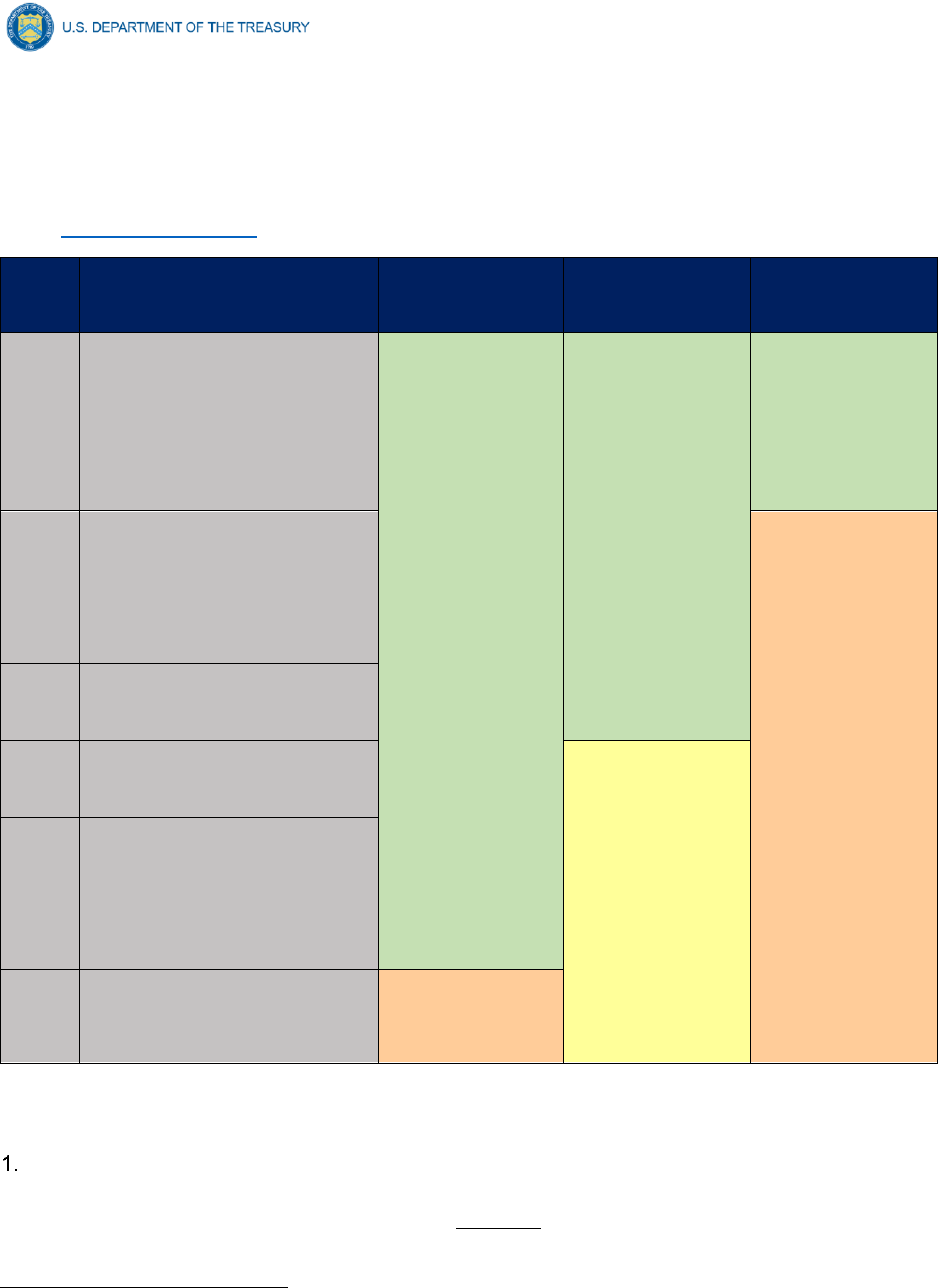

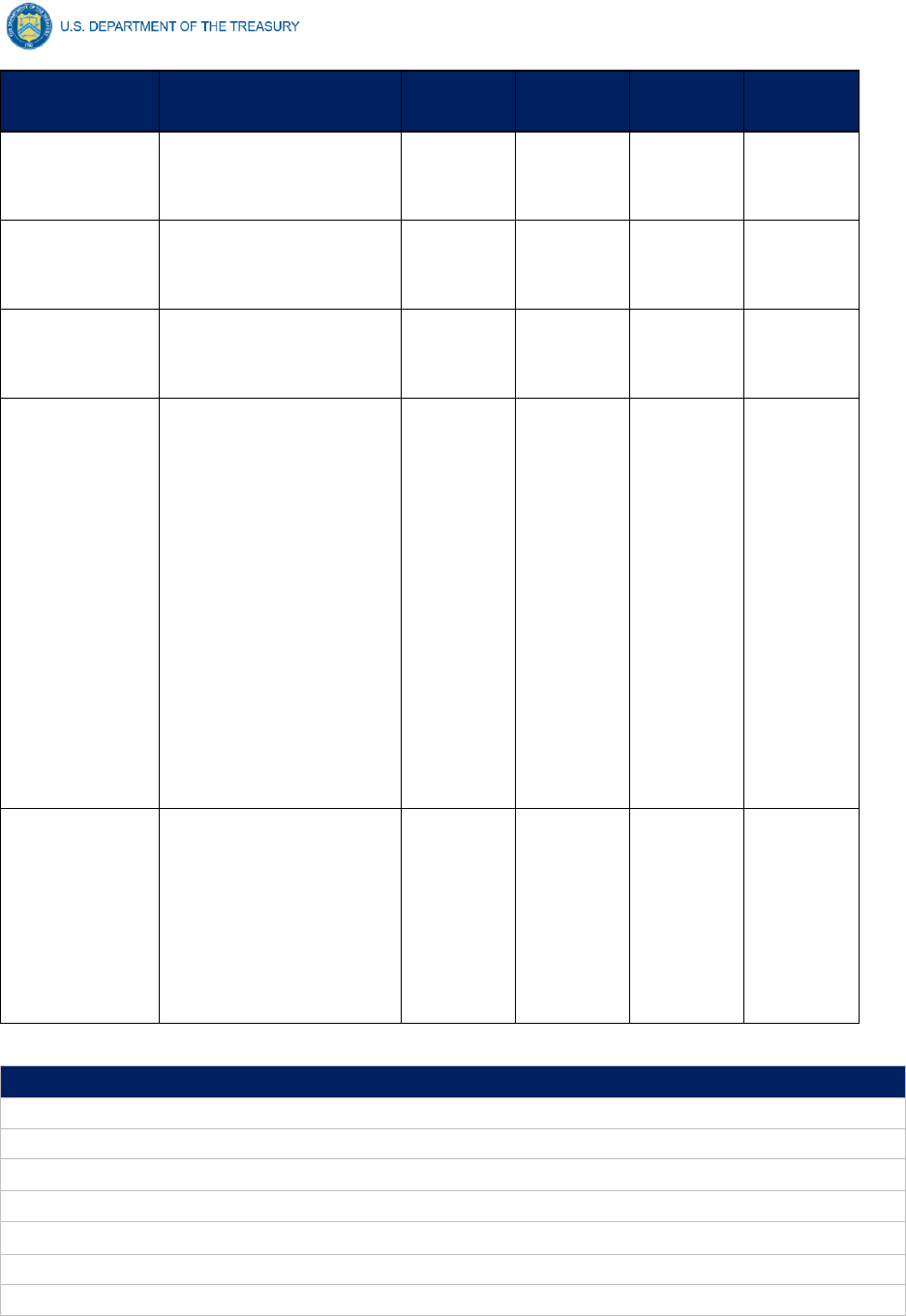

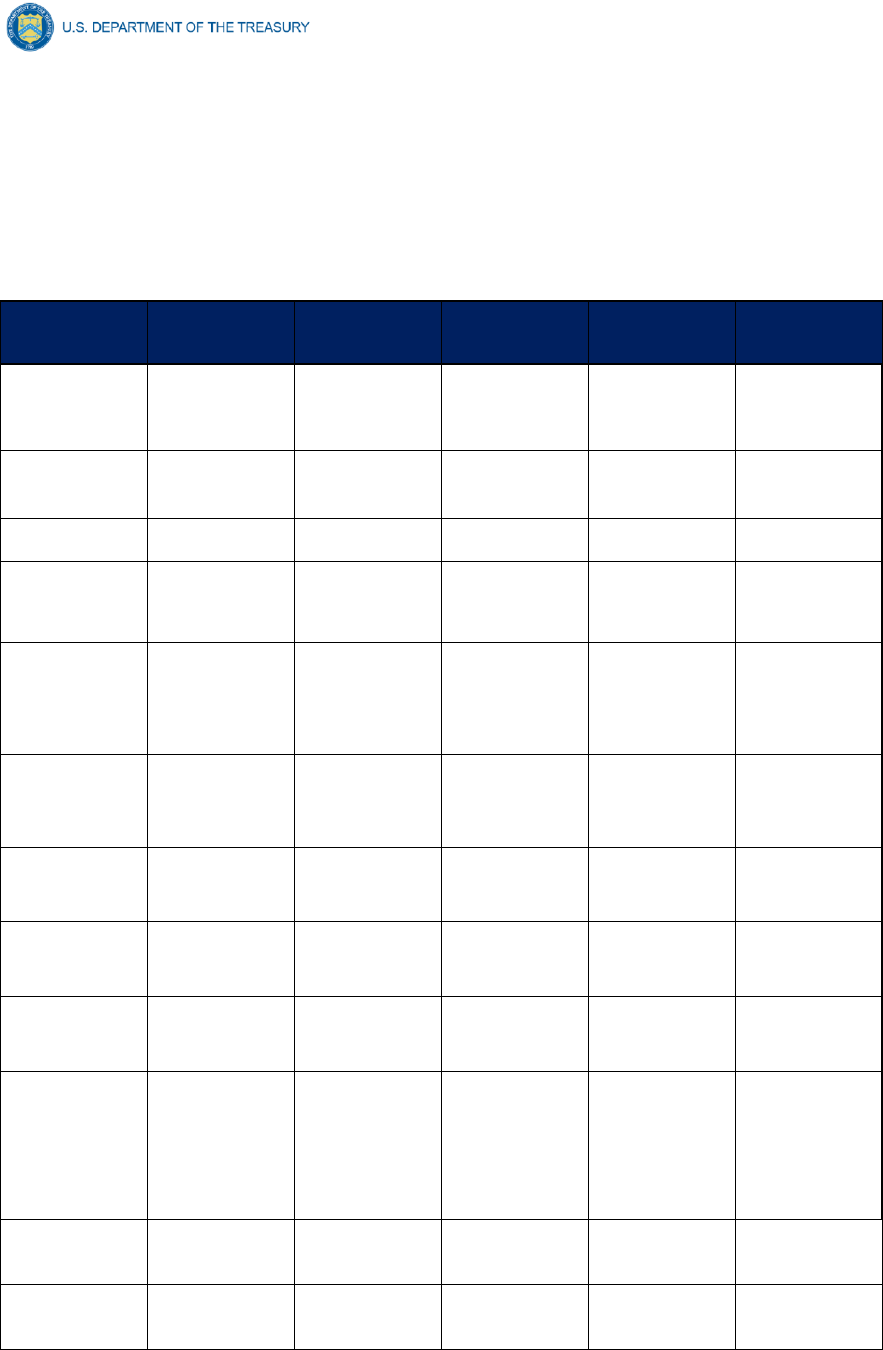

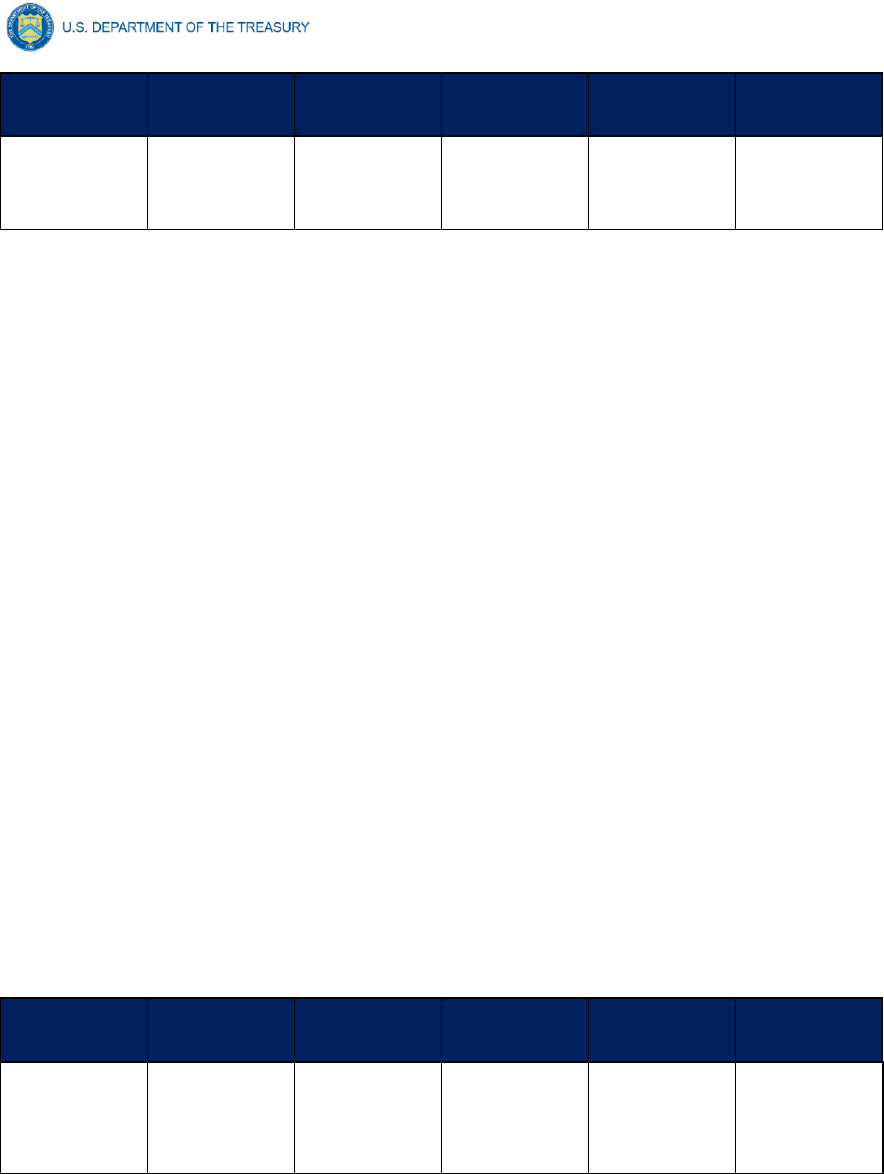

For the SLFRF program, reporting requirements vary by recipient type, as shown in the table

below. Detailed instructions for completion and submission of each report are covered in Part 2

of the Reporting Guidance.

Tier

Recipient

Interim Report

Project and

Expenditure

Report

Recovery Plan

Performance

Report

1

States, U.S. territories,

metropolitan cities and

counties with a population

that exceeds 250,000

residents

By August 31,

2021 or 60 days

after receiving

funding if

funding was

received by

October 15, with

expenditures by

category

By January 31,

2022, and then

30 days after the

end of each

quarter

thereafter

1

By August 31,

2021 or 60 days

after receiving

funding, and

annually

thereafter by

July 31

2

2

Metropolitan cities and

counties with a population

below 250,000 residents

which received more than

$10 million in SLFRF

funding

Not required

3

Tribal Governments which

received more than $30

million in SLFRF funding

4

Tribal Governments which

received less than $30

million in SLFRF funding

By April 30,

2022, and then

annually

thereafter

3

5

Metropolitan cities and

counties with a population

below 250,000 residents

which received less than

$10 million in SLFRF

funding

6

NEUs

Not required

b) Project and Expenditure Report Requirements

Quarterly Reporting

The following recipients are required to submit quarterly Project and Expenditure Reports:

• States, and U.S. territories

1

Interim final rule Page 111

2

Interim final rule page 112

3

Interim final rule Page 111

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 9

• Metropolitan cities and counties with population that exceeds 250,000 residents

• Metropolitan cities and counties with a population below 250,000 residents which received

more than $10 million in SLFRF funding

• Tribal Governments that received more than $30 million in SLFRF funding

For these recipients, the initial quarterly Project and Expenditure Report will cover the period

from March 3, 2021 to December 31, 2021 and must be submitted to Treasury by January 31,

2022. The subsequent quarterly reports will cover one calendar quarter and must be submitted

to Treasury within 30 calendar days after the end of each calendar quarter

States and territories should continue to submit the monthly NEU/Non-UGLG distribution

information through the separate module in Treasury’s Portal.

Annual Reporting

The following recipients are required to submit annual Project and Expenditure Reports:

• Tribal Governments that received less than $30 million in SLFRF funding

• Metropolitan cities and counties with a population below 250,000 residents which received

less than $10 million in SLFRF funding

• Non-Entitlement Units of Local Government (NEU). To facilitate reporting, each NEU will

need a NEU Recipient Number. This is a unique identification code for each NEU assigned

by the State or U.S. Territory to the NEU as part of its request for funding.

For these recipients, the initial Project and Expenditure Report will cover from March 3, 2021 to

March 31, 2022 and must be submitted to Treasury by April 30, 2022. The subsequent annual

reports will cover one calendar year and must be submitted to Treasury by April 30 each year.

c) Key Concepts for Reporting

The following concept structure applies to all report types:

Expenditure Categories

• Each recipient is required to report the obligations and expenditures by project

according to the corresponding Expenditure Category (EC). As noted in the

Reporting Guidance, there are a wide range of eligible uses of the SLFRF funds,

and Treasury must be able to track how funds are used by recipients for oversight

and transparency purposes. In addition, States, U.S. territories and metropolitan

cities and counties with a population over 250,000 also need to provide the

adopted budget for each project.

o An obligation is an order placed – such as a contract – and similar

transactions that require payment.

o An expenditure is when the service has been rendered or the good has been

delivered to the entity, and payment is due.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 10

o The adopted budget is the budget adopted for each project by a recipient

associated with SLFRF funds. Recipients will enter the Adopted Budget

based on information that exists currently in the recipient’s financial systems

and the recipient’s established budget process. Treasury understands that

recipients may use different budget processes. For example, a recipient may

consider a project budgeted once a legislature has appropriated funds;

whereas another recipient may consider a project budgeted at the moment

when the funds have been obligated. Note that Treasury is not approving or

pre-approving projects or budgets. Treasury will use this information to better

understand the intended impact, identify opportunities for technical

assistance, and understand the recipient’s progress in program

implementation. Treasury is also collecting additional descriptive information

about the budget process in order to better understand the context of

recipients’ budget processes.

• For each project, the recipient will be asked to select the appropriate Expenditure

Category based on the scope of the project (as described in Appendix 1 of the

Reporting Guidance). Projects should be scoped to align to a single Expenditure

Category.

• The Expenditure Categories are important not only for tracking projects and

expenditures, but also because for certain Expenditure Categories you will need to

provide additional programmatic data. You will see them referred to regularly

throughout the Reporting Guidance and in this User Guide with “EC” followed by a

number.

• Appendix C includes the full list of the 66 Expenditure Categories

4

, which refers to

the detailed level. For instance, 1.1 is the EC related to Public Health: 1.1 COVID-

19 Vaccination.

• While 66 Expenditure Categories are identified, they are a very broad categorization

– each Expenditure Category could include many different programs and activities.

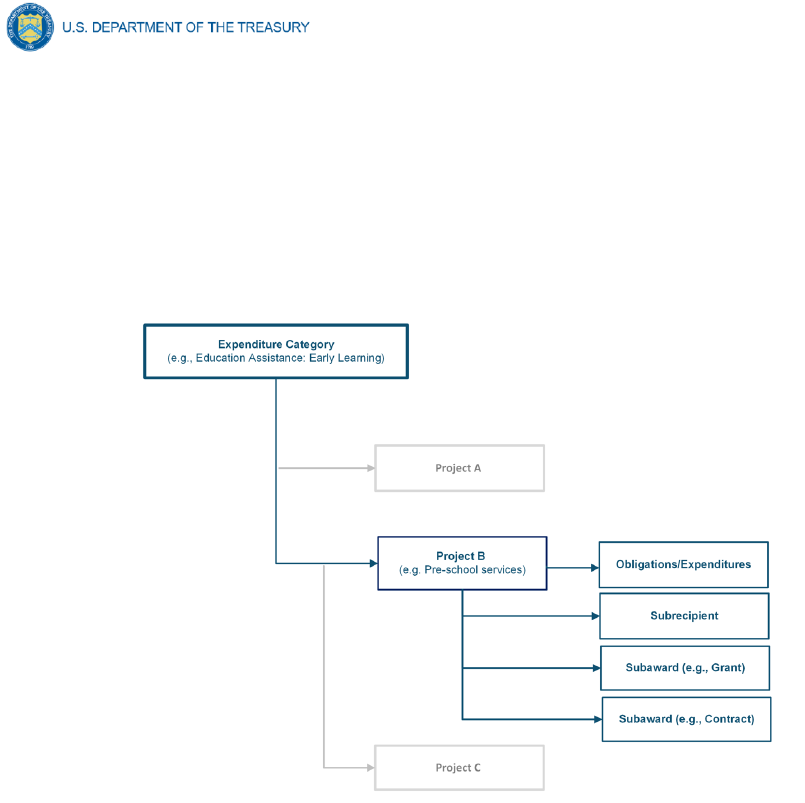

Project

• A project is defined as a grouping of closely related activities that together are

intended to achieve a specific goal or directed toward a common purpose.

• These activities can include new or existing services, funded in whole or in part by

the SLFRF award.

• Within this broad definition, recipients have flexibility to define their projects in a way

that provides the greatest clarity on the work which will be performed.

• Each project must align to one Expenditure Category. Projects break down an

Expenditure Category into more detail.

• You are required to define projects at a sufficient level of granularity to be able to do

any programmatic reporting that is required.

4

Included in Appendix 1 of the Reporting Guidance

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 11

• For each Expenditure Category you use funding for, you will have one or more

projects.

• For each project, you will need to track obligations and expenditures, as well as any

subawards made.

Figure 8 depicts the relationship between EC and multiple projects.

Figure 8 Relationship between Expenditure Categories and Multiple Projects

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 12

Section IV. Project and Expenditure Report

The Project and Expenditure Report provides information on projects funded, expenditures, and

contracts and subawards over $50,000, and other information required from recipients. Multiple

modules or “screens” will help navigate recipients through the Project and Expenditure Report in

Treasury’s Portal as follows:

a) Recipient Profile

b) Project Overview

c) Subrecipients/Beneficiaries

d) Subawards/Direct Payments

e) Expenditures

f) Recipient Specific

g) Certification

The following sections describe the reporting steps and information to be collected in each module.

a) Recipient Profile

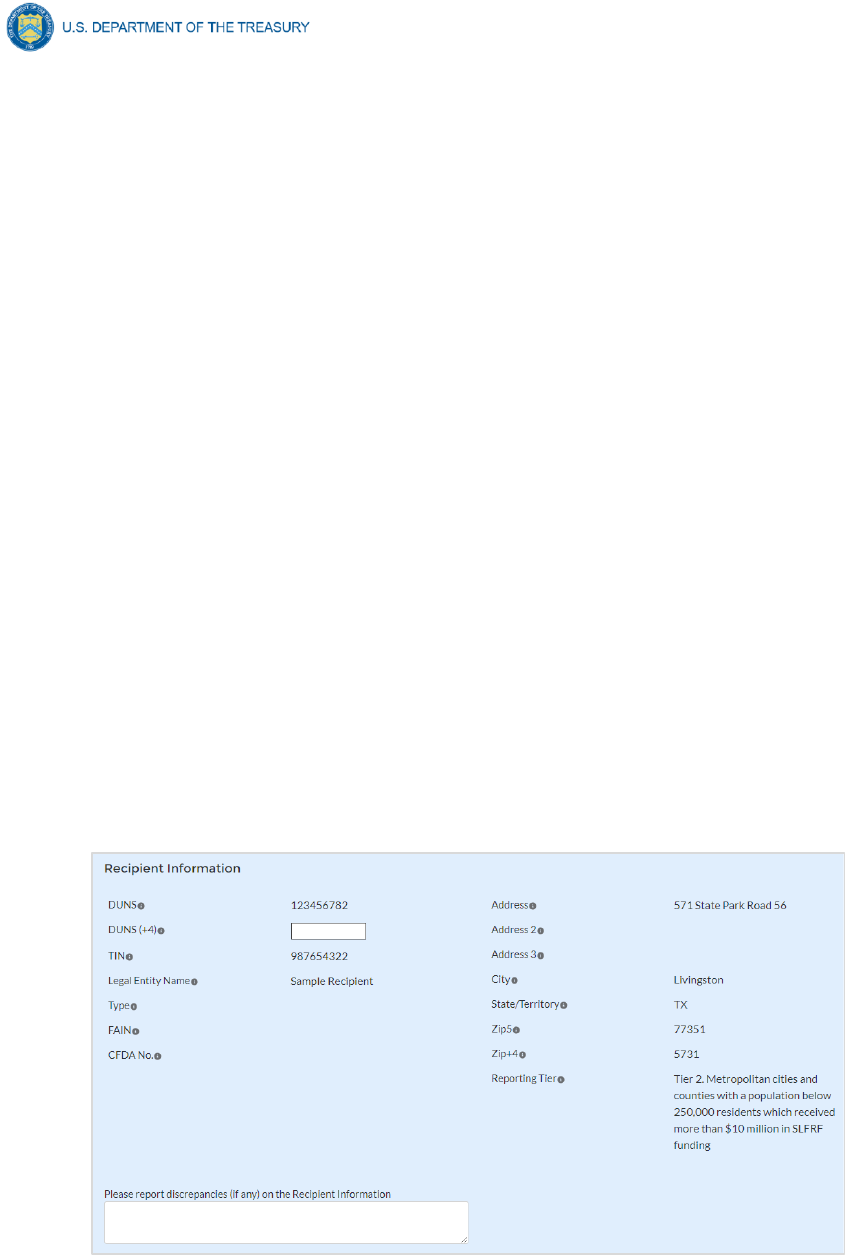

Upon login, you will be directed to the recipient information page, which is intended to verify

relevant information in Treasury’s Portal. On this screen, you will review and confirm key

information on your organization, and input information required for the Project and Expenditure

Report. Recipient Profile information will be pre-populated from your SLFRF Application file (see

Figure 11). If you have previously entered a DUNS (+4) number, it will appear here.

1. Review and confirm your Recipient Profile prepopulated from your SLFRF Application

file (see Figure 9).

2. If you have a Recipient DUNS (+4) number and the field is not populated, update as

necessary.

3. Verify the names and contact information for individuals the recipient has designated for

key reporting roles for the SLFRF program displayed on the screen (see Figure 10).

Figure 9 Recipient Information

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 13

Figure 10 Point of Contact List

If changes are needed to the information displayed on the screen, use the textbox (see Figure

11). Please refer to the instructions in Appendix A if the updates are associated with reporting

roles or contact SLFRP@treasury.gov.

4. For States, U.S. territories, and metropolitan cities and counties with a population over

250,000, provide the answers to the following two questions (see Figure 11):

• Who approves the budget in your jurisdiction? Select from the picklist as

follows: Legislature; Executive; Legislature & Executive; Other.

o If Other, specify who approves the budget. Please include information

about the role or function, not an individual’s name.

• Is your budget considered executed at the point of obligation? Select “Yes” or

“No”. Please note that if you select “Yes” and your budget is considered

executed at the point of obligation, then your adopted budget and total dollar

value of obligations for each project would be the same.

Figure 11 Budget Approval and Obligation

Treasury is requiring descriptive information about budget processes to support analysis

of adopted budget information. Treasury is collecting adopted budget information to

better understand the intended impact of recipient projects and help tell the story of how

these funds are used, identify opportunities for technical assistance, and understand the

recipient’s progress in program implementation. Treasury is requesting this descriptive

information to inform these efforts.

Treasury is not approving or pre-approving projects or budgets. Treasury also

recognizes that recipients may adjust project budgets over time, and recipients will have

the ability to reflect these changes in future reporting.

5. Complete the SAM.gov Registration and Executive Compensation information.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 14

a. Use the dropdown (see Figure 12) to confirm your entity’s SAM.gov status and

Executive Compensation reporting eligibility questions.

Figure 12 SAM.gov question

b. If you are registered in SAM.gov, select “Yes” from the picklist and move on to Step

6 below.

c. If you are not registered in SAM.gov, select “No” from the picklist. Two additional

questions will populate the space below (see Figure 13).

Figure 13 Additional SAM.gov questions (1)

d. If the recipient received 80% or more of its annual gross revenue from federal funds

AND the recipient received $25 million or more of its annual gross revenue from

federal funds, an additional question will appear (see Figure 14). If the answer is

“No” to any of these two questions, move on to step 6 below.

Figure 14 Additional Sam.gov questions (2)

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 15

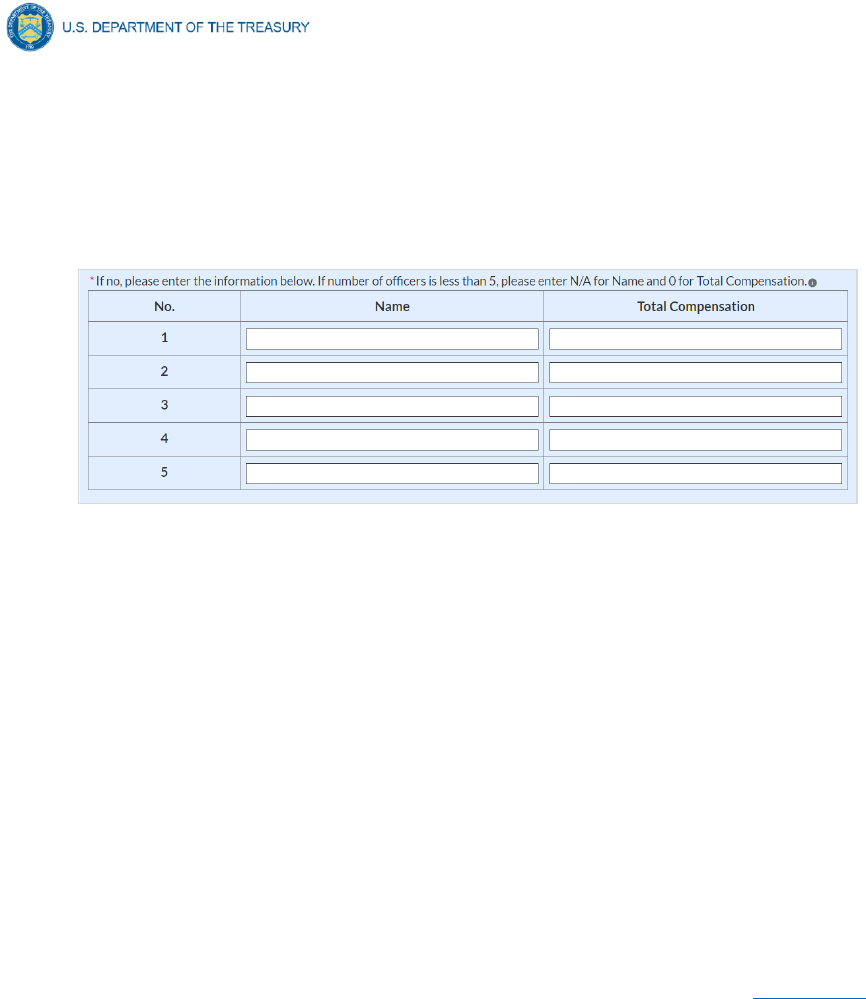

e. Select “Yes” if the total compensation for the organization’s five highest paid officers

is publicly listed or otherwise listed in SAM.gov and move on to Step 6 below.

f. Select “No” if the total compensation for the organization’s five highest paid officers

is not publicly listed or otherwise listed in SAM.gov. Enter the name(s) of the

officer(s) in the chart that will appear (see Figure 15) and the total compensation

received by each. If fewer than five (5) officers exist, enter “N/A” and $0 in the empty

field(s).

Figure 15 Record of Highest Paid Officer

6. Once all fields have been reviewed and verified, click the Save button to save your

progress, then click the Next button to proceed to the following screen.

b) Project Overview

Recipients are required to enter all projects funded through SLFRF funds as part of their Project

and Expenditure Report. Once projects are entered, they are viewable on the Project Overview

screen and can be updated in future reporting periods.

There are a couple of things to keep in mind when planning and executing your project

inventory entry:

• Manual versus Bulk Upload Entry: There are two ways to enter project information –

manual data entry and bulk upload. Bulk upload templates are specific to the project’s

expenditure category group. Recipients may upload information for multiple projects

within the same expenditure category group template simultaneously. Appendix B

provides step by step instructions for using the bulk upload option.

Due to the different data collected across expenditure categories, you should not use the

same bulk upload template from one expenditure category group to another.

• No Projects Available Option: If your jurisdiction has not yet identified any projects to

report, please know that maintaining a project list is a core requirement of the SLFRF

program.

For the Project and Expenditure Report due January 31, 2022, in the event recipients

have no projects available for entry, an option has been included in Treasury’s Portal to

allow recipients to select “No Projects Available” in lieu of adding projects not otherwise

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 16

approved. Selecting this option will require providing a written explanation and may

result in additional compliance follow-up from Treasury.

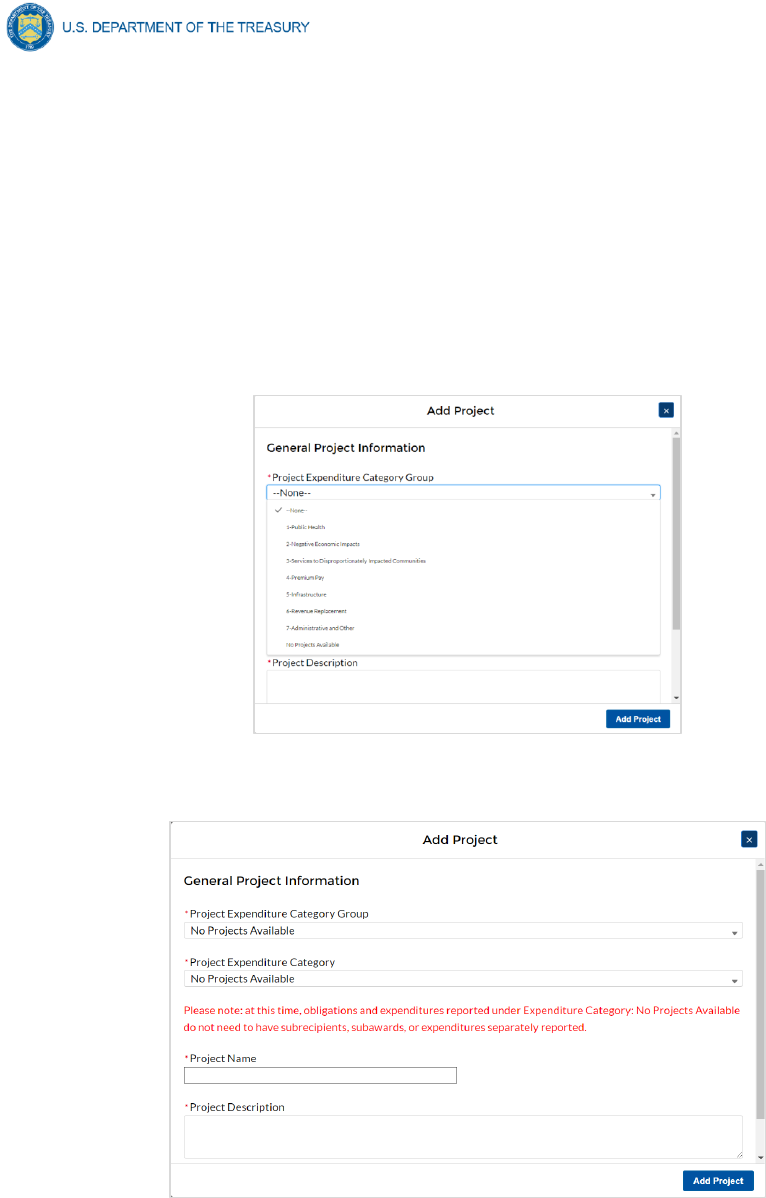

To utilize this option, on the Add Project screen

1. Select “No Projects Available” from the Project Expenditure Category Group

(See Figure 16).

2. Select “No Projects Available” from the Project Expenditure Category (see

Figure 17)

3. Enter in a Project Name of your choosing (See Figure 17).

4. Enter a description as to the rationale for no projects being available for

reporting.

Figure 16 No Projects Available Option

Figure 17 No Projects Available Entry Screen

• Non-Infrastructure and Infrastructure Projects Programmatic Data: Treasury

requests various programmatic data or impact measures for projects in several non-

infrastructure (i.e., projects in EC 1 – 4) and infrastructure projects (i.e., projects in EC

5.1 – 5.17). The programmatic data can be provided via manual project entry or via bulk

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 17

upload templates. Appendix B provides step by step instructions for using the bulk

upload option for projects with programmatic data. Appendix D provides additional detail

on the programmatic data requested by EC. Treasury recognizes that some

programmatic data may not be available until a project starts.

• Infrastructure Projects with expected total cost over $10M: Information for

infrastructure projects with expected total cost over $10 million must be entered

manually at this time in Treasury’s Portal. Appendix D provides additional detail on the

programmatic data requested by EC.

When creating infrastructure projects via bulk upload, it is important to re-open those

project records to manually complete fields related to costs over $10M.

• Transfers to NEUs (EC 7.4) (only applicable to States and U.S. territories): States

and U.S. territories should report any transfers to NEUs as part of the separate

NEU/Non-UGLG module. A project cannot be added under EC 7.4.

Recipients should refer to Appendix C when planning your project inventory entry, as it includes

a table identifying which ECs require the programmatic data. The table also maps each EC to its

appropriate bulk upload template.

All projects, regardless of Expenditure Category, require a set of “standard” data fields. Some of

these fields, such as project name and project ID, are static and do not change across reporting

periods. Other fields, such as status of completion and total obligations, will change across

reporting periods.

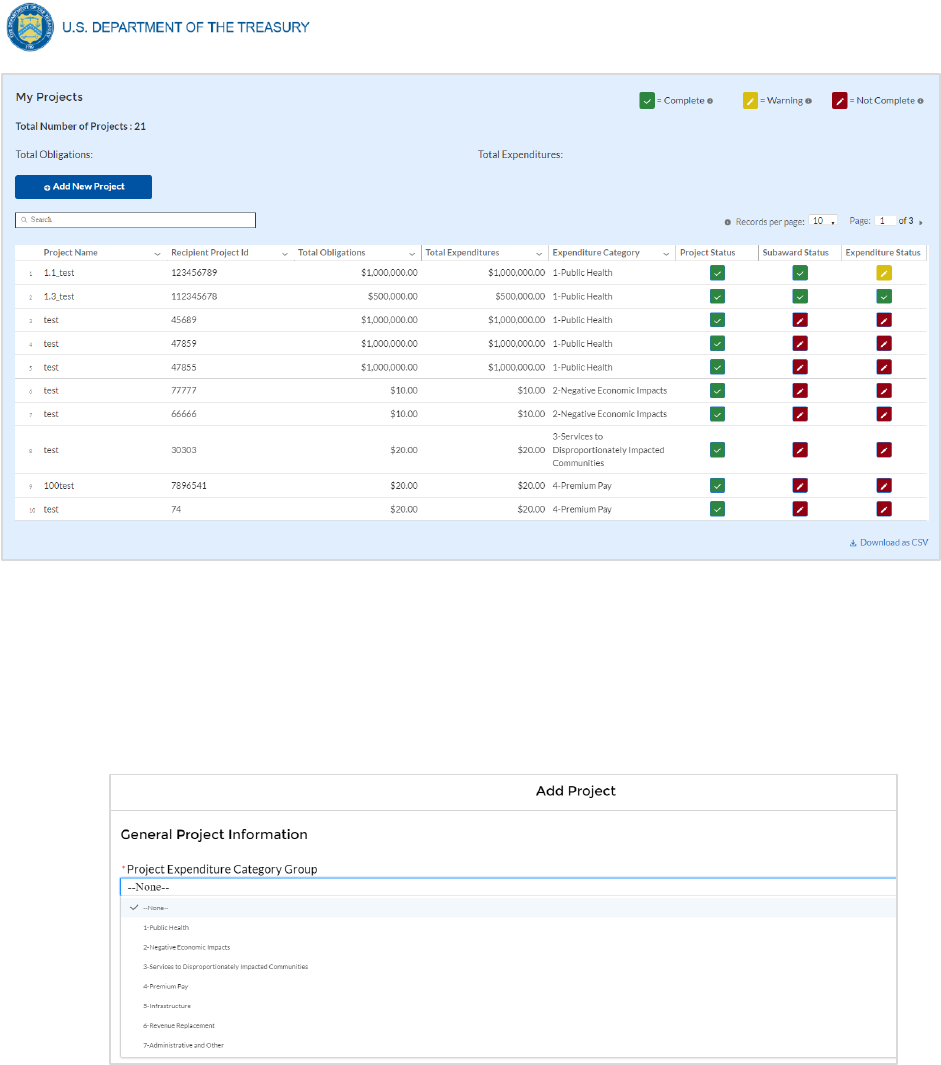

On the Project Overview Screen, recipients can view previously established projects and enter

new projects (see Figure 18). The screen displays the total number of projects and total

obligations for the recipient. The screen also displays the following for each project entered:

project name, project ID, adopted budget (if applicable), total obligations, total expenditures,

expenditure category, project status, subaward status, and expenditure status. To go directly to

a project to edit or add information, click the colored green or red status button for that project.

For Project Status, the green check icon indicates all required fields have been answered.

For Subaward Status and Expenditure Status, this indicates that at least one subaward or

expenditure entry has been made.

For Project Status, the yellow pencil icon indicates that the sum of all obligation or

expenditure amounts associated with the project is not equal to that project’s total obligations or

expenditures.

For Project Status, the red pencil icon indicates that not all required fields have been

answered. For Subaward Status and Expenditure Status, this indicates that no subaward or

expenditure entries have been made.

To add a new project from this screen, click the Add New Project button. You may need to

refresh your browser screen to see your previous new entries.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 18

Figure 18 My Projects Screen Example

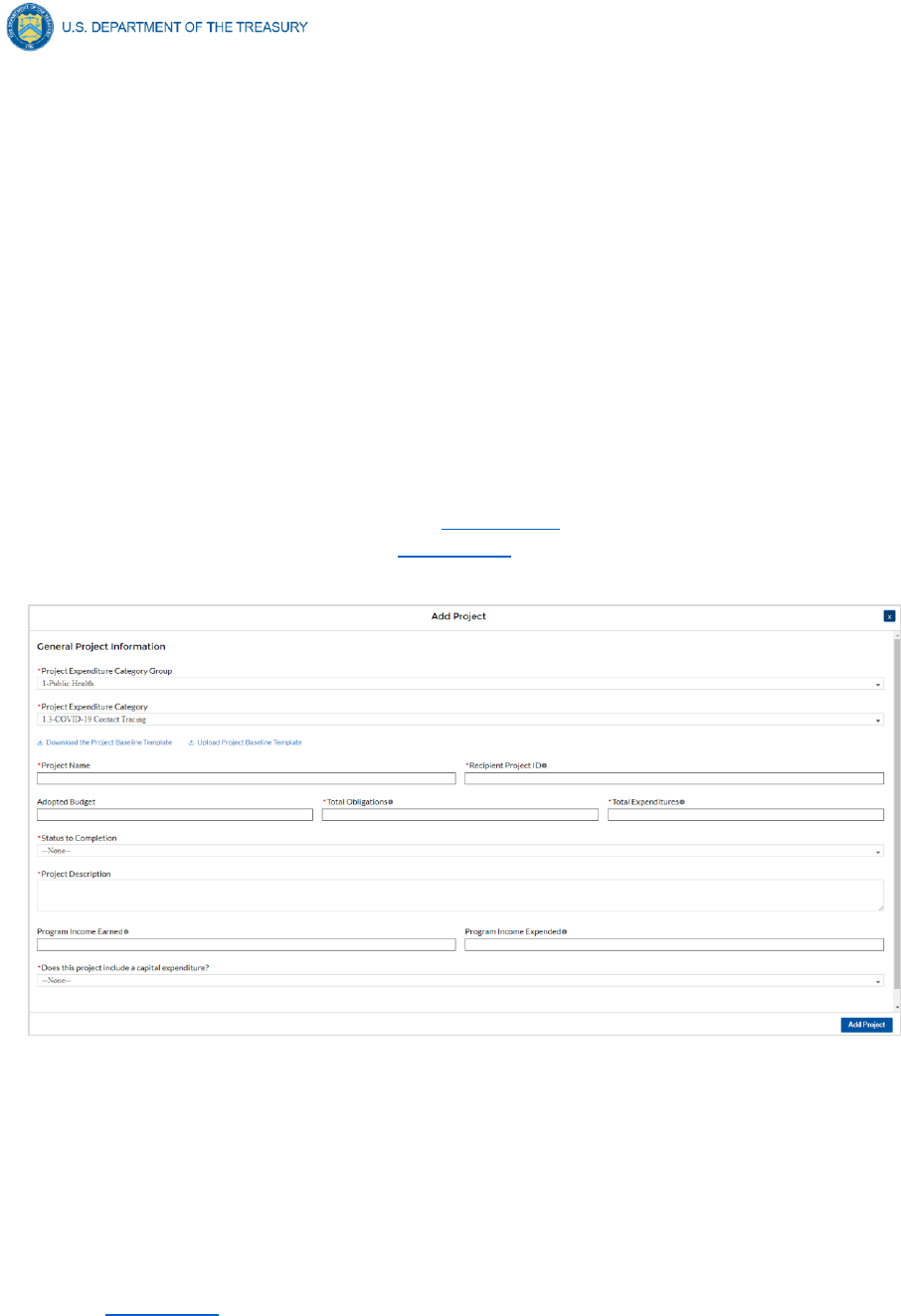

c) Add project manually

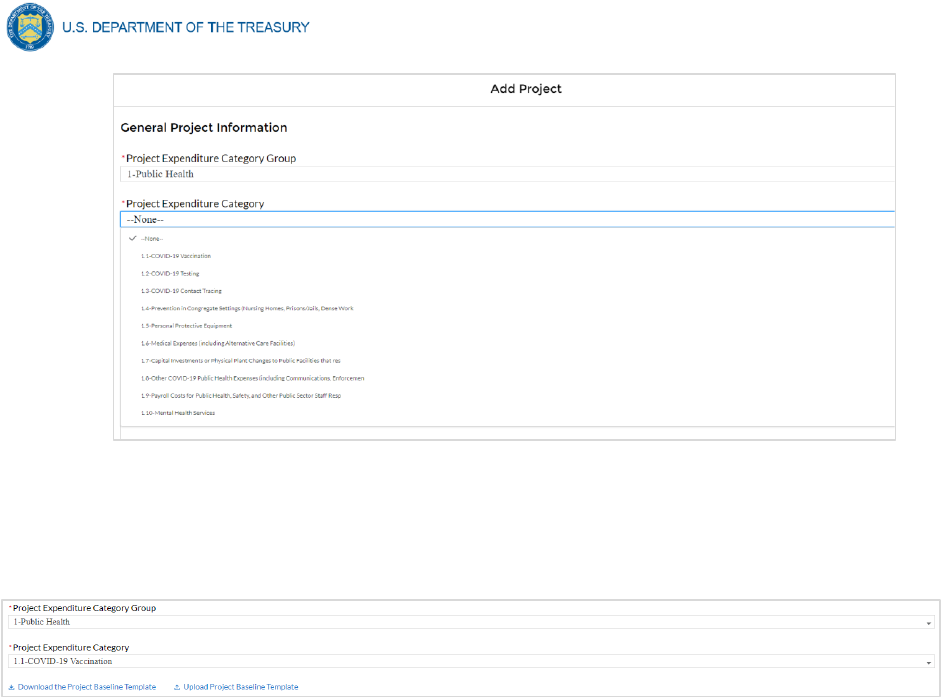

1. Select the Project Expenditure Category Group and Project Expenditure Category from

the picklists. Selection of Expenditure Category drives the template by which you will

manually enter the project data (see Figures 19 through 22). To view all of the ECs,

scrolling may be necessary.

Figure 19 Project Expenditure Category Group

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 19

Figure 20 Project Expenditure Category

2. Note that once you select values from the Project Expenditure Category Group and the

Project Expenditure Category picklists, the bulk download and upload links will appear

(see Figure 21). As you are entering the information manually, go to step 3.

Figure 21 Bulk Upload for EC 1.1

3. Enter the project name.

4. Enter the unique project identification number you assigned to the project. Do not use

duplicate project numbers for multiple projects.

5. Select the completion status of the project from the drop-down list. Options are:

• Not started

• Completed less than 50%

• Completed 50% or more

• Completed

6. For States, U.S territories and metropolitan cities and counties with population over

250,000, enter the adopted budget for the project.

7. Enter the total dollar value of obligations for this project. If funds have not been

obligated, enter "0".

8. Enter the total dollar value of expenditures for this project. If expenditures have yet to be

made, enter "0".

• Note – Recipients should ensure that Total Expenditures are less than or equal

to Total Obligations for each project. Treasury’s Portal will otherwise return an

error.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 20

9. Provide a description for the project between 50 to 250 words. Treasury encourages

recipients to include a description of the population they are serving, the desired impact,

and how this impact will be measured.

10. For projects reported under the Project Expenditure Categories EC1: Public Health,

EC2: Negative Economic Impact and EC3: Services to Disproportionately Impacted

Communities, provide answers to the questions “Does this project include a capital

expenditure”? If “Yes”, what is the total expected cost of the capital expenditure,

including pre-development costs? If the answer is “No”, include a zero for the expected

total cost of the capital expenditure.

11. If the project earns income or has expended that income, enter the total dollar value of

program income earned and Program income expended in the fields of the same name,

respectively. This field is optional.

12. If the project is in an EC which requires additional programmatic data, additional fields

will display on the screen. Please see Section IV.d below for more information on

providing programmatic data and Appendix D for more information on the programmatic

indicators themselves.

Figure 22 Project Entry Screen

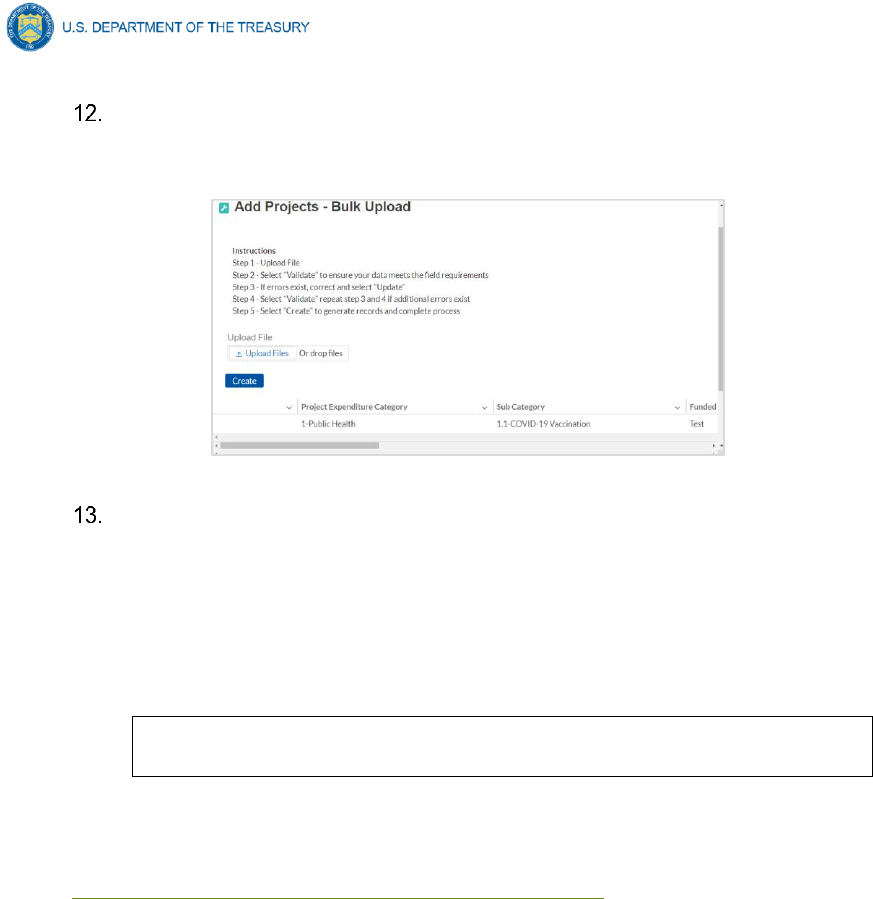

Once all of the above information is entered, click the Add Project button, then click the Next

button to proceed to the following screen or you can stay on this screen and continue adding

projects to your project inventory. Refer to Figure 22.

d) Programmatic Data for Projects

As noted above, projects in several ECs require programmatic data in addition to the standard

project information covered above and as described in Part B.3.i and B.3.j of the Reporting

Guidance. Appendix D provides additional detail on the measures and information required, by

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 21

Expenditure Category. This information should be provided at the project-level (e.g.,

disaggregated by project if the recipient has multiple projects in a single EC).

Programmatic data can be provided via the manual project entry process described above, or in

some cases via bulk upload using the Expenditure Category-specific templates, described in

Section IV.e and Appendix B.

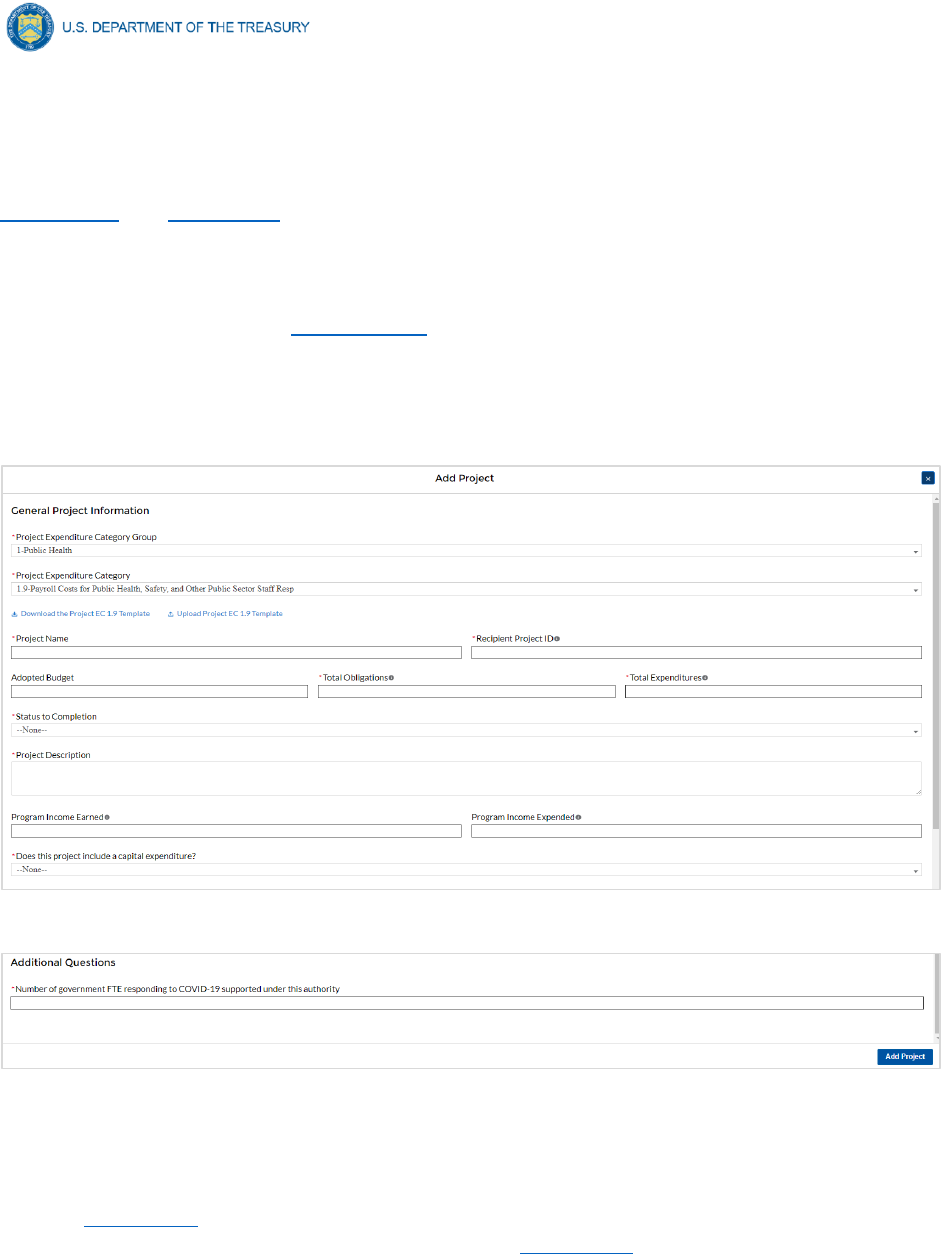

For example, to manually enter a new project in Expenditure Category 1.9 (see Figure 23)

Payroll Cost for Public Health, Safety, and other Public Sector Staff Resp, the recipient should:

1. Follow steps 1 – 11 in Section IV.c.1 above.

2. Populate the programmatic data field for “Number of government FTEs responding to

COVID-19 supported under this authority” (see Figure 24).

3. Once all of the above information is entered, click Add Project.

4. Click the Next button to proceed to the following screen.

Figure 23 Manual Entry for EC 1.9

Figure 24 Programmatic Data for EC 1.9

If entering projects via bulk upload, recipients should populate the programmatic data columns

contained in the appropriate EC’s bulk upload template.

Refer to Appendix D for a full listing of project Expenditure Categories with detail on the

additional information needed for specific categories. Appendix C provides a helpful table

mapping each Expenditure Category to the bulk upload template recipients should use if

inputting or updating projects via the bulk upload method.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 22

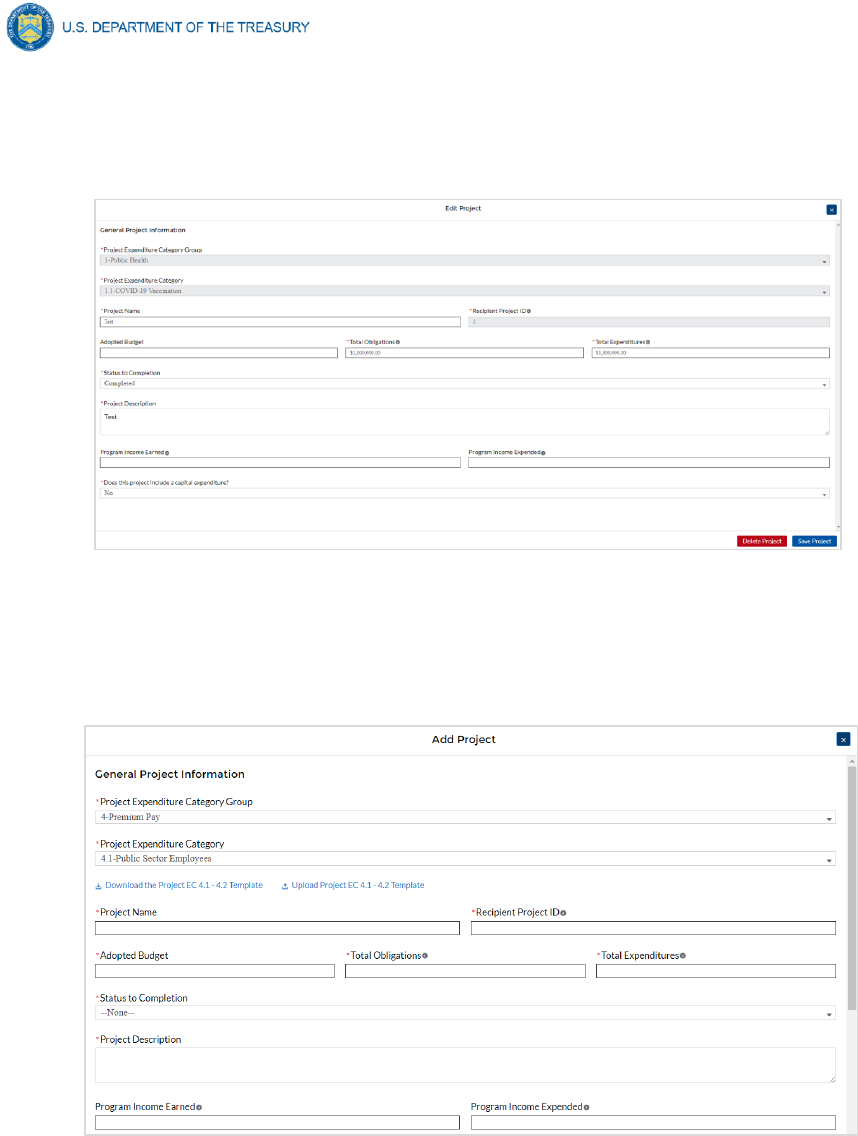

Projects entered into the system can be edited or deleted before final submission. To edit a

project, open the project from the My Projects screen. To delete a project, use the Delete

Project Button. If a report is already submitted, users will need to un-submit to edit or delete a

project record. See Figure 25.

Figure 25 Edit and Delete Project Screen

1. Premium Pay (EC 4.1 and EC 4.2)

If EC 4.1 or 4.2 is selected as the project expenditure category, recipients will need to provide

additional data.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 23

Figure 26 Premium Pay Screen and Additional Questions

In addition, recipients need to provide additional information in regard to Premium Pay, as

reflected in Figure 26.

Note - Recipients that are either creating or supporting a Premium Pay program may only

provide premium pay to eligible workers, e.g., workers needed to maintain continuity of

operations of essential critical infrastructure sectors (see sector list below), for essential work,

e.g., work that is not performed while teleworking from a residence; and involves either:

• regular, in-person interactions with patients, the public, or coworkers of the individual

that is performing the work; or

• regular physical handling of items that were handled by, or are to be handled by,

patients, the public, or coworkers of the individual that is performing the work.

• Sectors designated as essential critical infrastructure sectors: Recipients should refer to

the list of sectors below when providing information for this question. Recipients may also

refer to this list of sectors on the Subaward screens (see section IV.g) to answer the

question: Employer sector for all subawards to third-party employers (i.e., employers other

than the State, local, or Tribal government).

Sectors Designated as Essential Critical Infrastructure Sectors

Any work performed by an employee of a State, local, or Tribal government;

Behavioral health work;

Biomedical Research;

Dental care work;

Educational work, school nutrition work, and other work required to operate a school facility;

Election’s work;

Emergency response;

Family or childcare;

Grocery stores, restaurants, food production, and food delivery

Health care;

Home- and community-based health care or assistance with activities of daily living;

Laundry work;

Maintenance work;

Medical testing and diagnostics;

Pharmacy;

Public health work;

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 24

Sectors Designated as Essential Critical Infrastructure Sectors

Sanitation, disinfection, and cleaning work;

Social services work;

Solid waste or hazardous materials management, response, and cleanup work;

Transportation and warehousing;

Vital services to Tribes;

Work at hotel and commercial lodging facilities that are used for COVID-19 mitigation and containment;

Work in a mortuary;

Work in critical clinical research, development, and testing necessary for COVID-19 response.

Work requiring physical interaction with patients;

Other

Beyond this list, the chief executive (or equivalent) of a recipient government may designate

additional non-public sectors as critical so long as doing so is necessary to protecting the health

and wellbeing of the residents of such jurisdictions.

Premium Pay Narrative: Premium pay must be responsive to eligible workers performing

essential work during the public health emergency. For groups of workers that do not meet one

of the two criteria below, Recipients must submit a written justification to Treasury describing

how the premium pay or grant is responsive to workers performing essential work during the

public health emergency:

1. Eligible worker receiving premium pay is earning (with the premium included) below 150

percent of their residing state or county’s average annual wage for all occupations, as

defined by the Bureau of Labor Statistics Occupational Employment and Wage

Statistics

5

, whichever is higher, on an annual basis; or

2. Eligible worker receiving premium pay is not exempt from the Fair Labor Standards Act

overtime provisions.

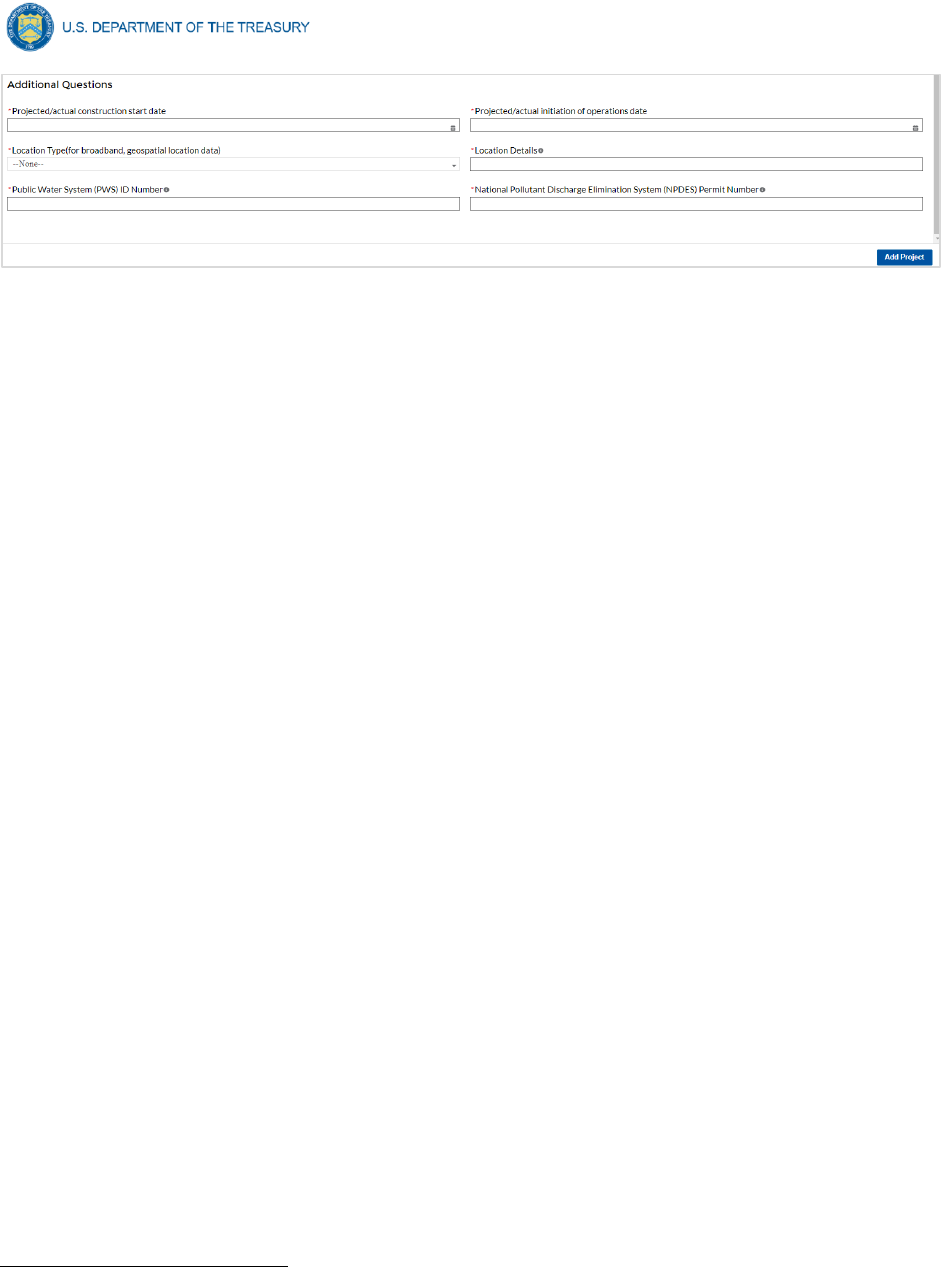

2. Infrastructure Projects Programmatic Data (EC 5)

Programmatic data is requested for Infrastructure projects in addition to data uploaded by bulk

template. That additional programmatic data can only be entered manually at this time in

Treasury’s Portal.

If adding an infrastructure project via the bulk upload method, recipients will be asked to provide

additional data in Treasury’s Portal screens manually (see Figure 27 for example of a project

providing water or sewer services). Alternatively, recipients can enter all infrastructure project

information manually. Reference Appendix D for detailed information on infrastructure project

entry and the Reporting Guidance for more general information on infrastructure project entry.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 25

Figure 27 Programmatic Data for Infrastructure Projects

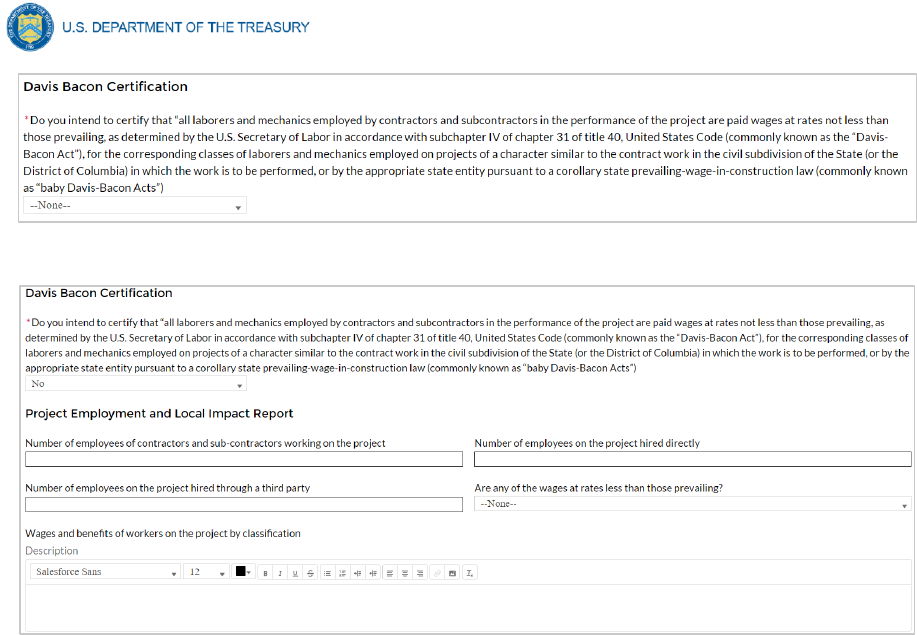

3. Infrastructure Projects with total expected costs over $10M

Recipients entering infrastructure projects with total expected costs over $10 million are

required to respond to two questions manually. If you expect a project to exceed $10 million

over its lifetime, it is strongly recommended to complete the certifications in advance to avoid

future retroactive reporting burden and project-associated expenses.

Recipients are required to provide the following two certifications, or provide additional

information:

a) Davis Bacon Act Certification (see Figures 28 and 29):

1) Select “Yes” or “No” response to Certification question for compliance with Davis-

Bacon Act: Do you intend to certify that “all laborers and mechanics employed by

contractors and subcontractors in the performance of the project are paid wages

at rates not less than those prevailing, as determined by the U.S. Secretary of

Labor in accordance with subchapter IV of chapter 31 of title 40, United States

Code (commonly known as the “Davis-Bacon Act”), for the corresponding

classes of laborers and mechanics employed on projects of a character similar to

the contract work in the civil subdivision of the State (or the District of Columbia)

in which the work is to be performed, or by the appropriate state entity pursuant

to a corollary state prevailing-wage-in-construction law (commonly known as

“baby Davis-Bacon Acts”)?

2) If response is “No”, enter the following information in the revealed questions:

i. The number of employees of contractors and sub-contractors working on

the project;

ii. The number of employees on the project hired directly and hired through

a third party; and

iii. The wages and benefits of workers on the project by classification; and

iv. Whether those wages are at rates less than those prevailing

6

.

PLEASE NOTE: Selecting "Yes" to 1(a) means that you intend to certify that all contractors and

subcontractors are paying prevailing wages and fringe benefits to all laborers and mechanics on

the project.

6

As determined by the U.S. Secretary of Labor in accordance with subchapter IV of chapter 31 of title 40,

United States Code (commonly known as the “Davis-Bacon Act”), for the corresponding classes of

laborers and mechanics employed on projects of a character similar to the contract work in the civil

subdivision of the State (or the District of Columbia) in which the work is to be performed.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 26

Figure 28 Davis Bacon Certification

Figure 29 Additional Questions if Response to Davis Bacon Certification is "No"

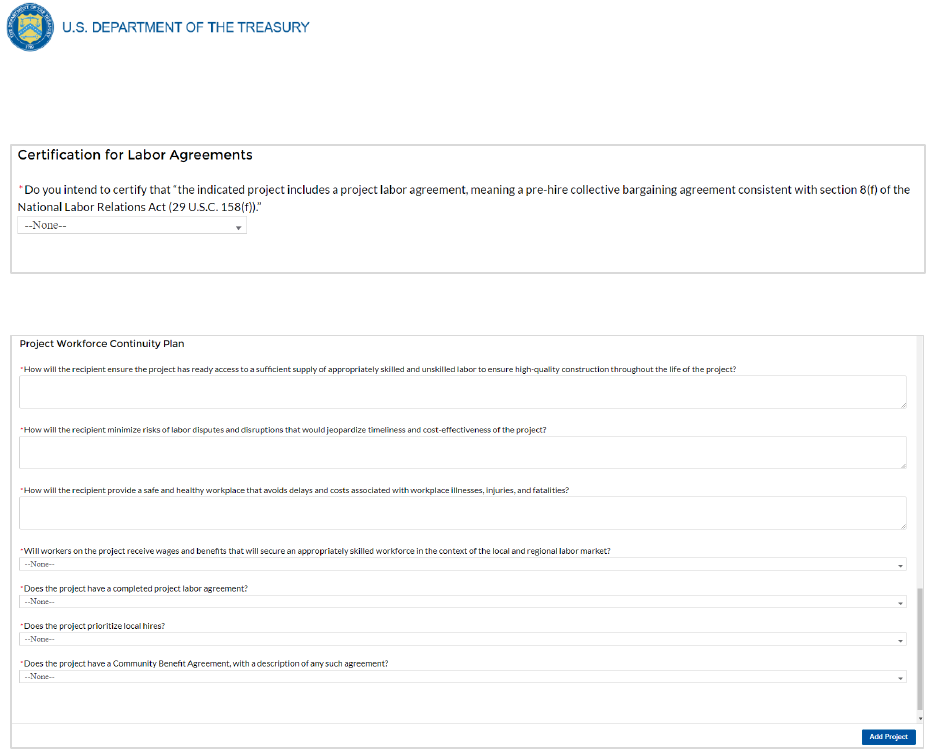

b) Project Labor Agreement Certification (Figures 30 and 31):

1) Select “Yes” or “No” response to Certification question for existence of project

labor agreement: Do you intend to certify that “the indicated project includes a

project labor agreement, meaning a pre-hire collective bargaining agreement

consistent with section 8(f) of the National Labor Relations Act (29 U.S.C.

158(f))?

2) If response is “No”, enter the following information about a project continuity plan

in the pop-up window:

i. How the recipient will ensure the project has ready access to a sufficient

supply of appropriately skilled and unskilled labor to ensure high-quality

construction throughout the life of the project, including a description of

any required professional certifications and/or in-house training;

ii. How the recipient will minimize risks of labor disputes and disruptions that

would jeopardize timeliness and cost-effectiveness of the project;

iii. How the recipient will provide a safe and healthy workplace that avoids

delays and costs associated with workplace illnesses, injuries, and

fatalities, including descriptions of safety training, certification, and/or

licensure requirements for all relevant workers (e.g., OSHA 10, OSHA

30);

iv. Whether workers on the project will receive wages and benefits that will

secure an appropriately skilled workforce in the context of the local or

regional labor market; and

v. Whether the project has completed a project labor agreement.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 27

PLEASE NOTE: Selecting "Yes" to 2(a) means that you intend to or are using an 8(f) pre-hire

agreement on your project.

Figure 30 Certification for Labor Agreements

Figure 31 Additional Questions if response is "No"

Once all of the above information is entered, click Add Project. Click the Next button to proceed

to the following screen.

4. Water and sewer projects (EC 5.1-5.15)

Recipients will provide information associated with water and sewer projects, under EC 5.1

through 5.15 when the project starts. Recipients are not required to provide the information if the

project has not started. When the “Status of Completion” field is marked “Not Started, the

additional questions required for water and sewer projects will not populate.

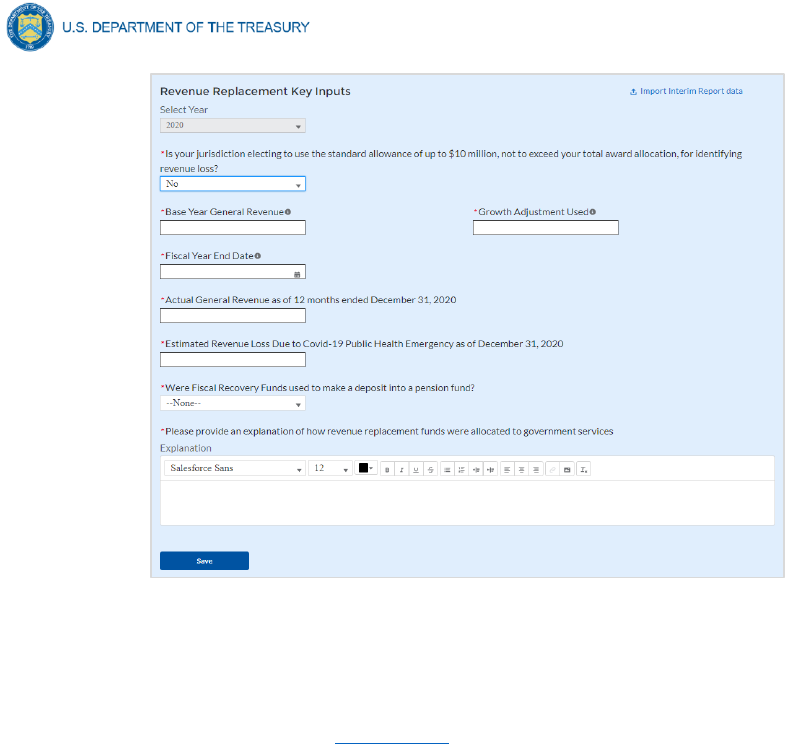

5. Revenue Replacement

Recipients will have the option to update or provide information associated with revenue

replacement not previously provided as part of prior submissions. Information previously

provided as part of the Interim Report (if provided) will display in this screen. Depending on

your answer to the question, “is your jurisdiction electing to use the standard allowance of up to

$10 million for identifying the revenue loss?” you will be asked conditional questions. Refer to

Figure 30.

As outlined in the final rule, Recipients will have the option to make a one-time decision to

calculate revenue loss according to the formula outlined in the final rule or elect a “Standard

Allowance” of up to $10 million, not to exceed the award allocation, to spend on government

services throughout the period of performance.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 28

For recipients calculating revenue loss according to the formula, note that the final rule permits

recipients are permitted to choose whether to use calendar or fiscal year calculation dates.

Recipients must use the same calculation time frame (calendar or fiscal year) throughout the

award period.

For recipients electing the “Standard Allowance,” Treasury will presume that up to $10 million,

not to exceed the award allocation, in revenue has been lost due to the public health emergency

and recipients are permitted to use that amount to fund “government services.” Please note that

electing the standard allowance does not change a recipient’s total allocation.

Treasury’s Portal will allow all recipients to elect to use this standard allowance instead of

calculating lost revenue using the formula. Refer to Figure 32. The following question will

display in the screen for all recipients, including those with total allocations of $10 million or less:

• Is your jurisdiction electing to use the standard allowance of up to $10 million, not to

exceed your total award allocation, for identifying revenue loss? Yes/No (Please note

electing the standard allowance does not change your total allocation).

Based on the recipient’s election, certain information will display in Treasury’s Portal which the

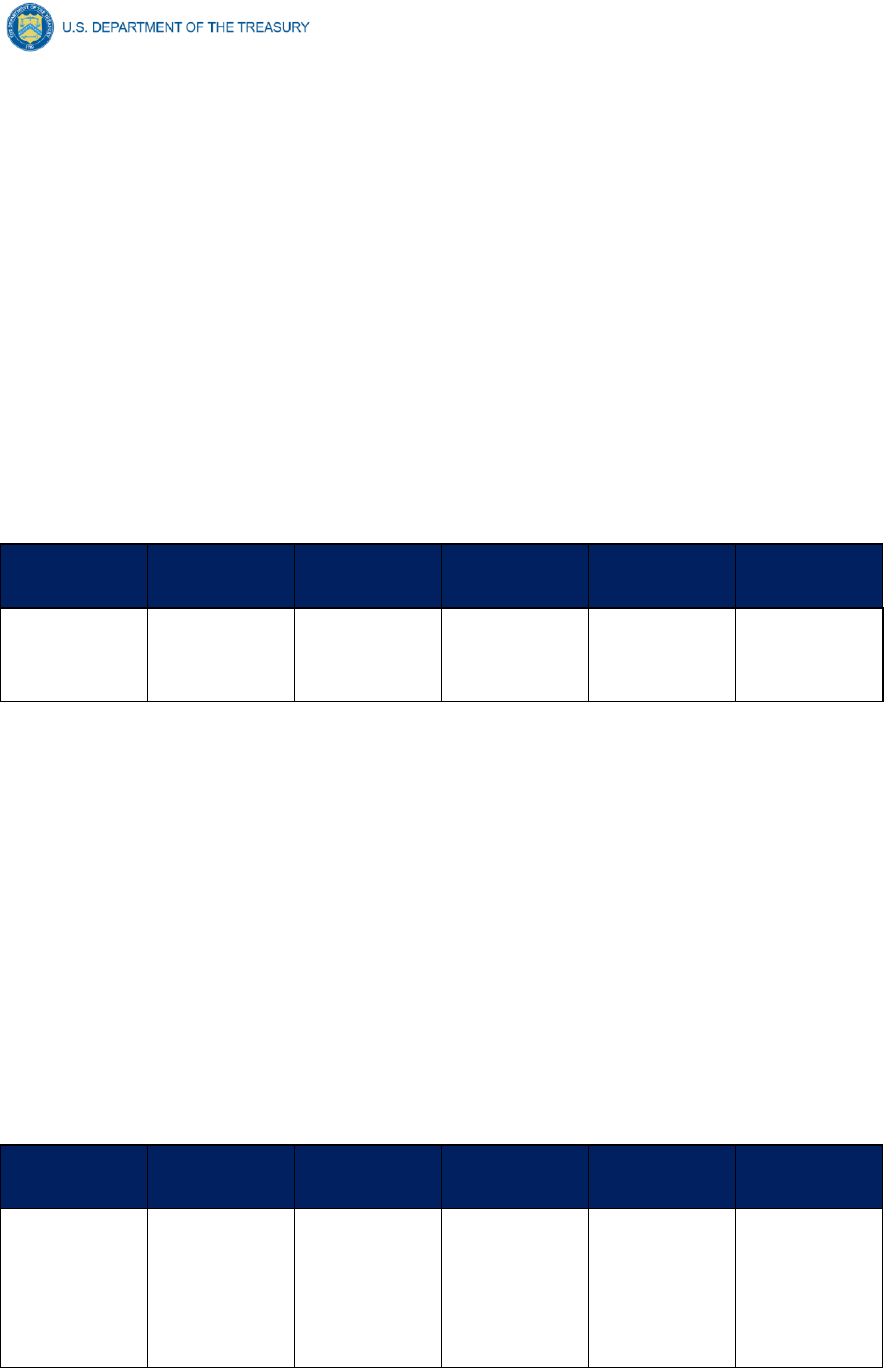

recipient will need to complete, as noted in the table below:

Data

Standard Allowance – Yes

Standard Allowance- No

Base Year Revenue

N/A

Required

Fiscal Year End Date

N/A

Required

Growth Adjustment Used

N/A

Required

Actual General Revenue as of 12

months ended December 31, 2020

N/A

Required

Estimated Revenue Loss

N/A

Required

Select whether Fiscal Recovery Funds

were used to a make a deposit into a

pension fund. Please note that no

recipients except for Tribal governments

may use Fiscal Recovery Funds to

make a deposit to a pension fund

Required

Required

Provide an explanation of how revenue

replacement funds were allocated to

government services: Please provide an

explanation

Required

Required

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 29

Figure 32 Revenue Replacement Screen

e) To enter projects using the bulk upload method:

Recipients have the option to provide project information via bulk upload, in lieu of manual entry

for some or all of their projects. Please note, bulk upload templates are specific to the EC the

project best aligns to. The table in Appendix C provides a mapping of project ECs to their

appropriate bulk upload template.

1. Fill the downloaded template with information specific to each project’s EC, as follows.

Projects within the same EC or set of ECs covered by a given template can be uploaded

together. For example, all projects in EC 2.1 to 2.5 (Negative Economic Impacts) can be

entered together on the Project Bulk Upload for Project EC 2.1-2.5 Template. Optional

fields are denoted by (*). “Column” below refers to the applicable area in the bulk upload

file.

• Column B: Select the Project Expenditure Group

• Column C: Select the Project Expenditure Category

• Column D: Enter the Project Name

• Column E: Enter the unique project identification number assigned by the

State or U.S. Territory to the project. Do not use duplicate project numbers for

multiple projects

• Column F: Select the completion status of the project

• Column G: Enter the total dollar value of the adopted budget for this project *

(only applicable to States, U.S. Territories, and metropolitan cities and

counties with population over 250,000)

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 30

• Column H: Enter the total dollar value of obligations for this project. If no

amounts are obligated, enter “0”

• Column I: Enter the total dollar value of expenditures for this project. If no

expenditures have been incurred, enter “0”

• Column J: For projects in EC 1, EC 2, or EC 3, enter a yes or no response to

the question, does this project include a capital expenditure?

• Column K: If yes, what is the total expected cost of the capital expenditure?

• Column L: Enter a description of the project

• Column M: Enter the amount of Federal program income earned

• Column N: Enter the amount of that was used to cover eligible project costs

• Column O: Enter a brief description of the structure and objectives of

assistance program(s) (e.g., nutrition assistance for ow income households)

• Column P: Enter the number of households served (by program if recipient

establishes multiple separate household assistance programs)

• Column Q: Enter a brief description of recipient’s approach to ensuring that

aid to households responds to a negative economic impact of Covid-19.

2. Upload the Project Entry and Status template, in this case the template for EC 2.1-2.5,

separately as a .csv file by using the respective Upload button on the screen or dropping

the files in this view.

3. Once all of the above information is entered, click Add Project. Click the Next button to

proceed to the following screen.

Refer to Appendix B for additional information related to the bulk file upload process

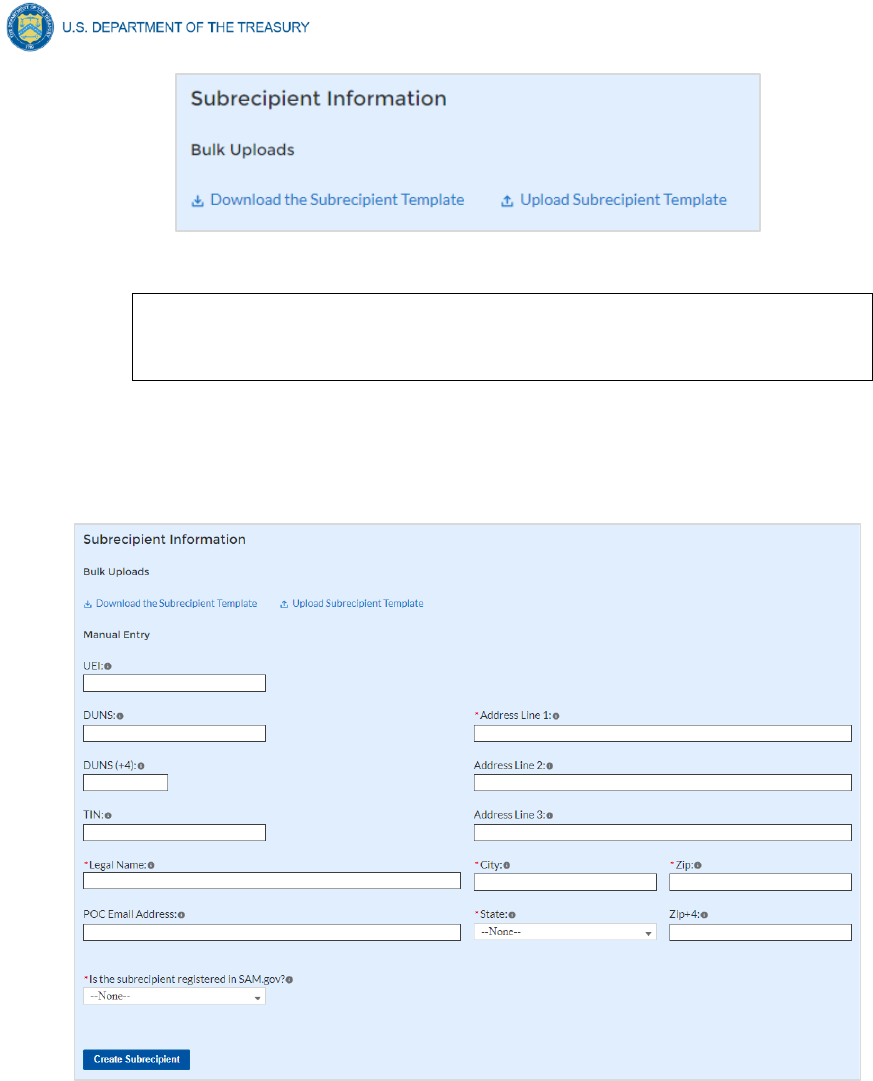

f) Subrecipients or Beneficiaries

The Subrecipients or Beneficiaries Profile documents the information about each subrecipient or

beneficiary that has received at least one Subaward or Direct Payment of federal funding greater

than $50,000 to execute projects supporting the SLFRF program. Please note that projects

entered under EC 6.1 Provision of Government Services are not required to enter Subrecipient,

Subaward, or Expenditures (for a subaward) information for the January reporting cycle. The

Subrecipients or Beneficiaries module allows users to enter data manually or leverage the bulk

file upload capability. For bulk-upload instructions specific to this submodule, see Appendix B.

You can download the bulk file template for use in submitting the required data via bulk upload.

When ready to submit the data, use the upload button (see Figure 33).

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 31

Figure 33 Subrecipient Bulk Upload Icon

Note: When using the bulk file upload capability, the Subrecipient bulk

upload must be completed prior to beginning the data entry for the

Subawards module.

If you choose to individually enter records, follow the instructions below.

1. Enter the relevant Subrecipient or Beneficiary information in each of the required fields

(see Figure 34). Recipients must enter at least one of the following three identifiers for a

subrecipient: UEI (Unique Entity Identifier), DUNS, or TIN.

Figure 34 Manually Create a Subrecipient or Beneficiary

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 32

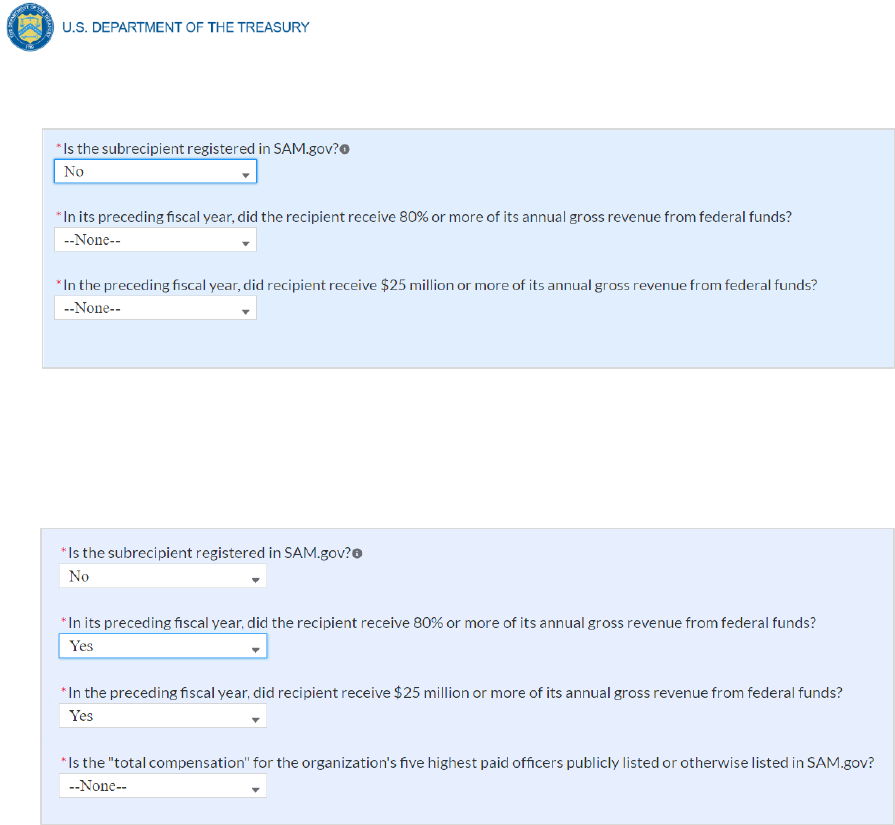

2. If the subrecipient or beneficiary is not registered in SAM.Gov, select “No” from the

picklist. Two additional questions will populate the space below (see Figure 35).

Figure 35 Sam.gov Questions for Subrecipients

3. If the recipient received 80% or more of its annual gross revenue from federal funds

AND the recipient received $25 million or more of its annual gross revenue from federal

funds, an additional question will appear (see Figure 36).

Figure 36 Additional SAM.gov questions for Subrecipients

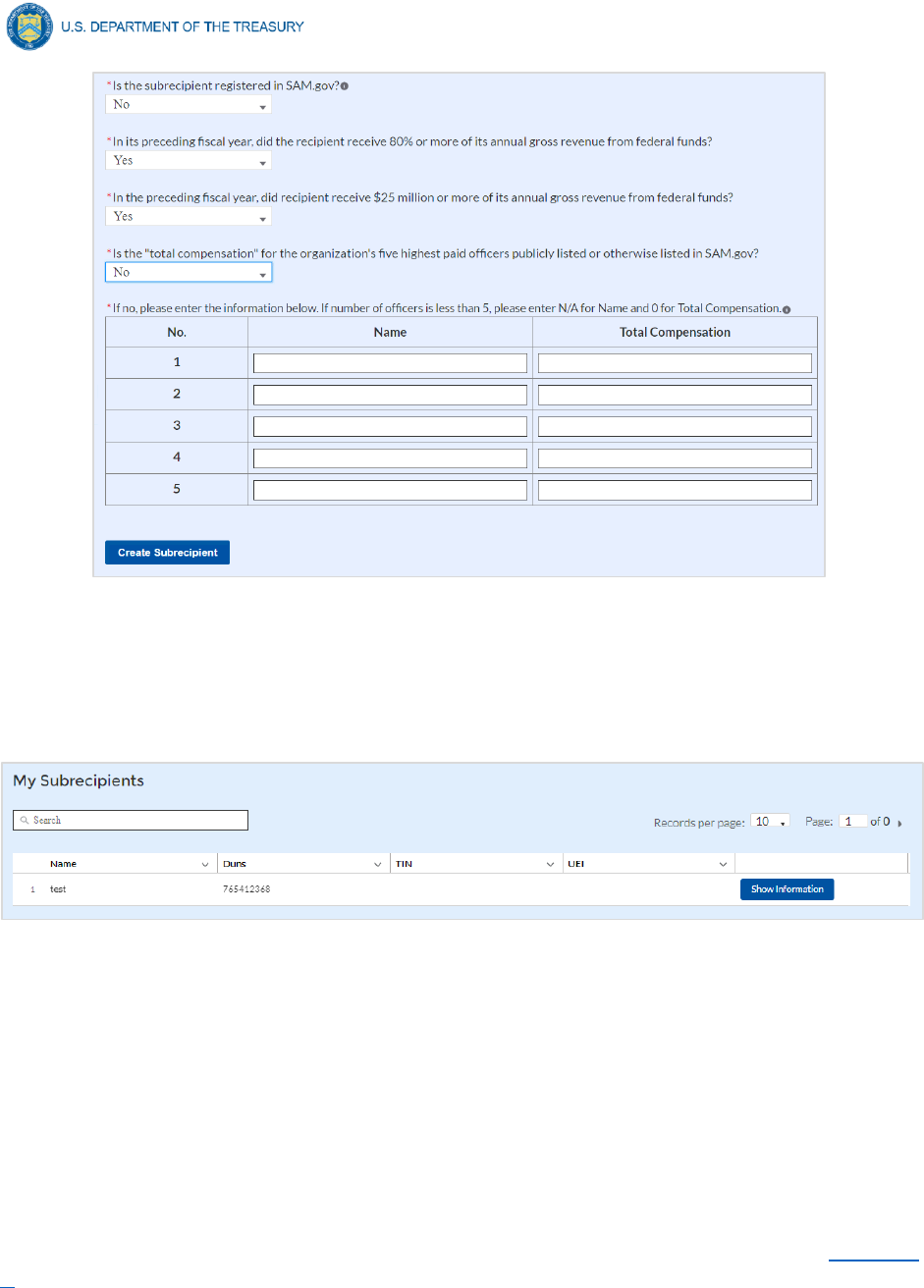

4. Select “Yes” if the total compensation for the organization’s five highest paid officers is

publicly listed or otherwise listed in SAM.Gov and move on to step 6 below.

5. Select “No” if the total compensation for the organization’s five highest paid officers is

not publicly listed or otherwise listed in SAM.Gov. Enter the name(s) of the officer(s) in

the chart that will appear (see Figure 37) and the total compensation received by each. If

fewer than five (5) officers exist, enter “N/A” and $0 in the empty field(s).

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 33

Figure 37 Five Highest Paid Officers for Subrecipients or Beneficiaries

6. At the bottom of the page, click the Create Subrecipient icon to complete the

Subrecipient record and return to Subrecipient screen.

7. Subrecipient or Beneficiaries entered into the system are shown at the bottom portion of

the screen (see Figure 38).

Figure 38 Subrecipients Entered

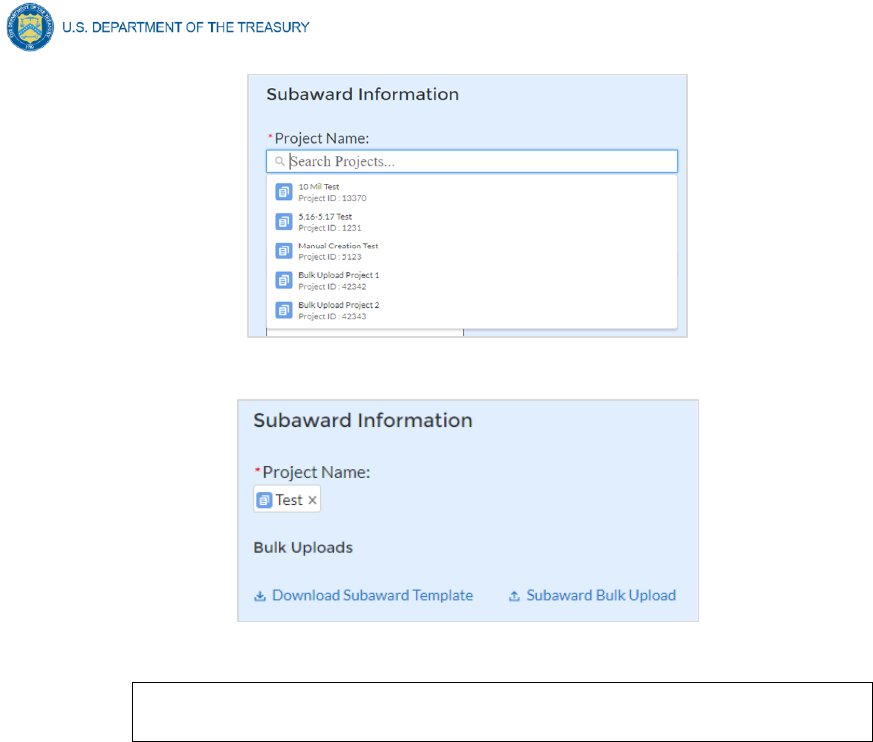

g) Subawards or Direct Payments

The Subawards or Direct Payments section allows recipients to enter the required information

regarding Subawards or Direct Payment of federal funding greater than $50,000 for all direct

payments, subawards, and contracts made by your organization under SLFRF. Please note that

projects entered under EC 6.1 Provision of Government Services are not required to enter

Subrecipient, Subaward, or Expenditures (for a subaward) information for the January reporting

cycle.

The Subawards or Direct Payments module allows users to enter data manually or leverage the

bulk file upload capability. For bulk-upload instructions specific to this submodule, see Appendix

B. You can download the bulk template using the provided link in Treasury’s Portal before using

the upload button (see Figures 39 and 40).

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 34

Figure 39 Subaward Bulk Upload (1)

Figure 40 Subaward Bulk Upload (2)

Note: Subaward bulk upload can only be completed after Subrecipient bulk

upload is completed.

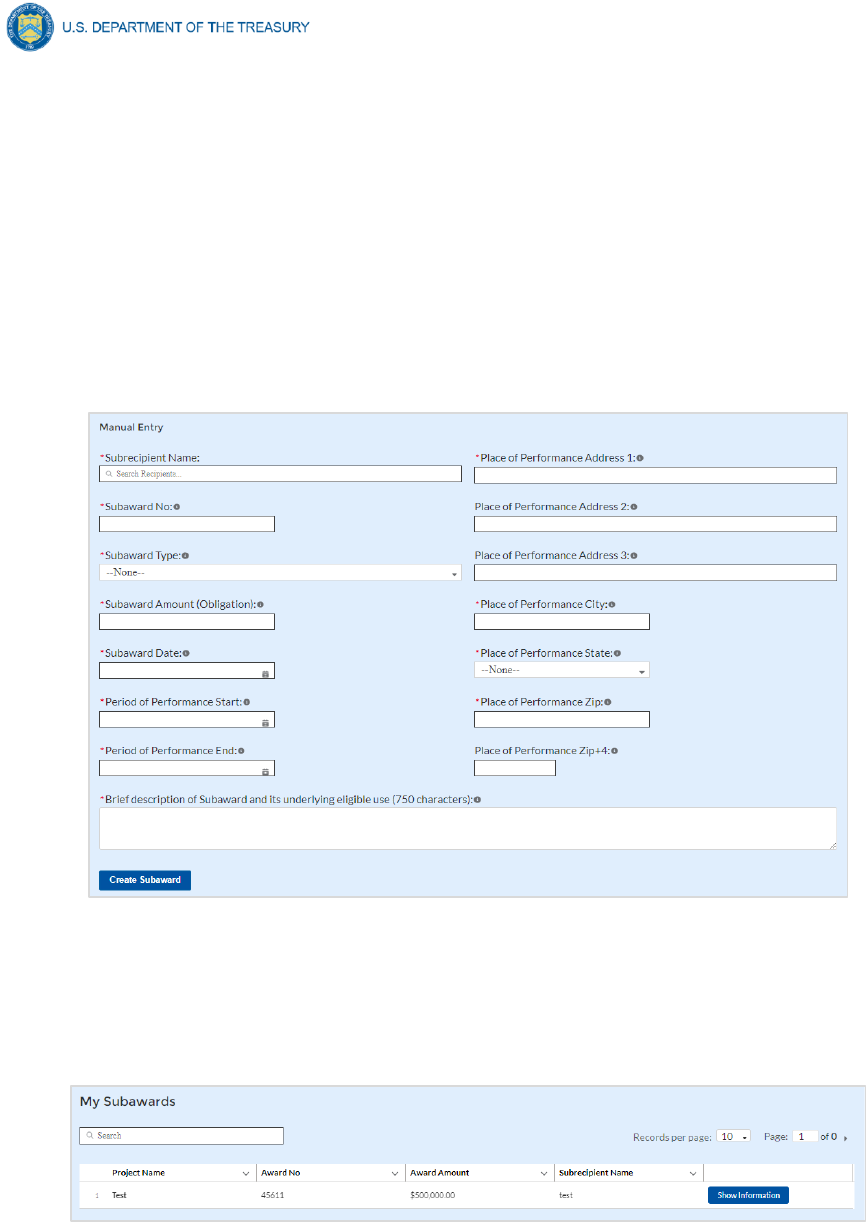

If you choose to individually enter records, follow the instructions below.

1. Enter the following fields pertaining to the Subawards or Direct Payments (see Figure

41):

• Subrecipient or Direct Payment Recipient Name from the picklist

• Subaward Number

• Subaward Amount (Obligation)

• Subaward Date

• Period of Performance Start

• Period of Performance End

• Place of Performance Address, City, State, Zip, Zip+4

2. Select the Subaward Type from the drop-down picklist:

• Contract: Purchase order

• Contract: Delivery order

• Contract: Blanket Purchase Agreement

• Contract: Definitive contract

• Grant: Lump sum Payment(s)

• Grant: Reimbursable

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 35

• Loan - Maturity prior to 12/31/26 with planned forgiveness (please see note

below on use of loans)

• Loan - Maturity prior to 12/31/26 without planned forgiveness (please see note

below on use of loans)

• Loan - Maturity past 12/31/26 with planned forgiveness (please see note below

on use of loans)

• Loan - Maturity past 12/31/26 without planned forgiveness (please see note

below on use of loans)

• Direct Payment

• Transfer: Lump Sum Payment(s)

• Transfer: Reimbursable

Figure 41 Subaward Reporting

3. Click Create Subaward to establish the Subaward record. Repeat Steps 1 through 3 to

create additional Subaward records.

4. Subawards entered into the system are shown at the bottom portion of the screen (see

Figure 42).

Figure 42 Subaward Entered

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 36

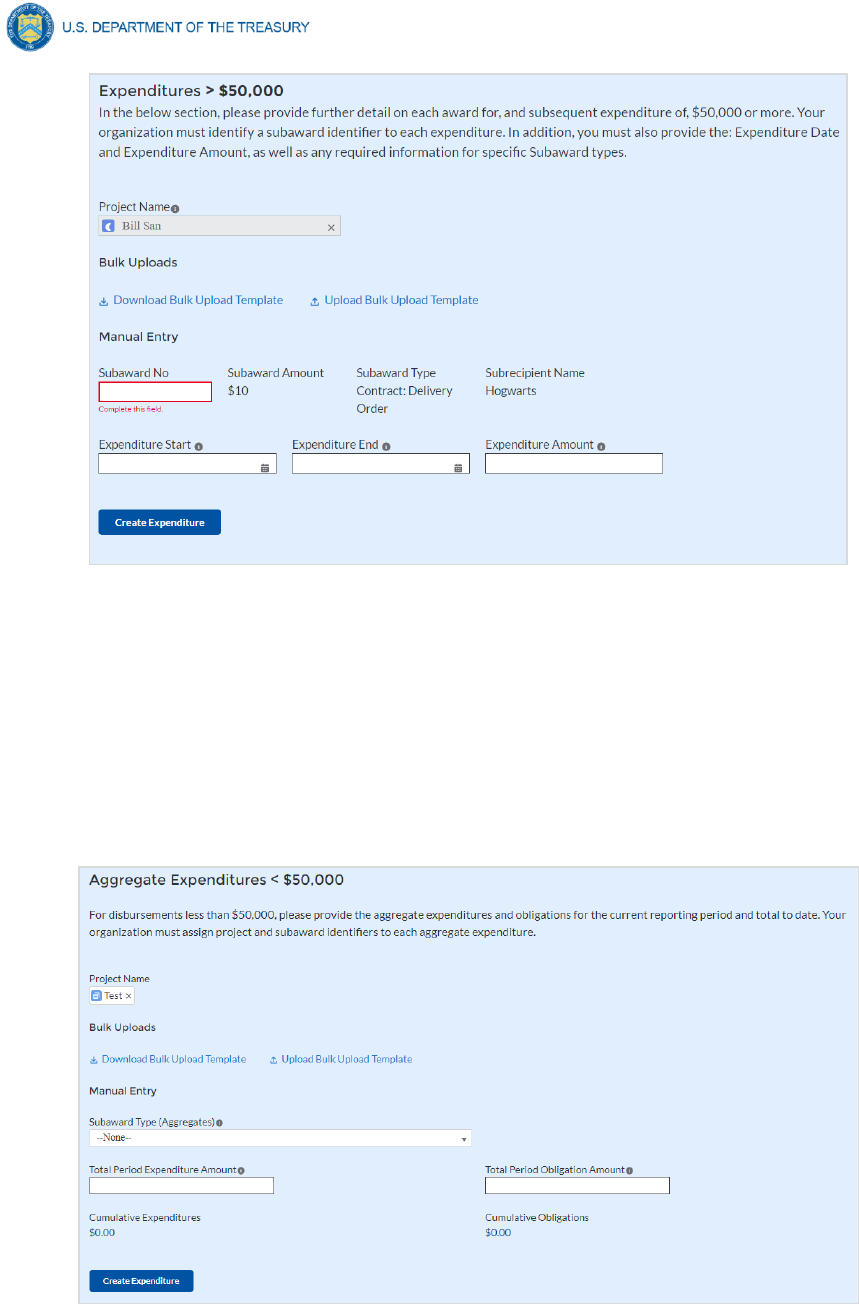

h) Expenditures

In the Expenditures tab, recipients will provide information for each contract, grant, loan,

transfer, or direct payment greater than $50,000. Additionally, aggregate reporting is required

for contracts, grants, transfers made to other government entities, loans, direct payments, and

payments to individuals that are less than $50,000. If aggregated expenditures linked to a

project equal the total Expenditures reported for that project, the Subaward status box on the

My Projects screen is changed to ‘Complete’. Please note that projects entered under EC 6.1

Provision of Government Services are not required to enter Subrecipient, Subaward, or

Expenditures (for a subaward) information for the January reporting cycle.

The Expenditures reporting module allows users to enter data manually or leverage the bulk file

upload capability. For bulk-upload instructions specific to this submodule, see Appendix B.

If you do not use the bulk upload function, follow the steps listed below.

1. To report new expenditures under a specific subaward, enter the subaward number.

The Project Name associated with the subaward will auto populate.

2. Enter the following:

• Expenditure Start Date

• Expenditure End Date

• Expenditure Amount

3. Enter narrative for Administrative Costs, if applicable.

4. Click the Create Expenditure button to submit the record. Repeat Steps 1 through 6 to

report additional sub-award expenditures. Proceed to the next segment once all sub-

award expenditures are reported.

1. Expenditures Greater than $50,000

For expenditures for awards greater than $50,000, fill out the “Expenditures for Awards>

$50,000” box (see Figure 43). Project name and subaward will be selected to link each

expenditure to the appropriate entries. Note that the Project name is automatically identified

based on the associated Subaward No. entered. Once the information has been entered, click

the Create Expenditure button on the bottom left of the box.

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 37

Figure 43 Expenditures >$50,000

Alternatively, the Expenditures for Awards greater than $50,000 bulk upload template (Figure

43) may be used and uploaded with the relevant information.

2. Expenditures Less than $50,000

For expenditures for awards less than $50,000 fill out the “Aggregate Expenditures < $50,000”

box (see Figure 44). Once the information has been entered, click the Create Expenditure

button on the bottom left of the box. Note the need to manually identify the Project Name as no

Subaward is necessary for Aggregate Expenditures less than $50,000.

Figure 44 Aggregated Expenditures <$50,000

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 38

Aggregate subaward types available for selection are as follows.

• Aggregate of Contracts Awarded

• Aggregate of Grants Awarded

• Aggregate of Loans Issued

• Aggregate of Transfers

• Aggregate of Direct Payments

Alternatively, the Aggregate Expenditures less than $50,000 bulk upload template may be used

and uploaded with the relevant information.

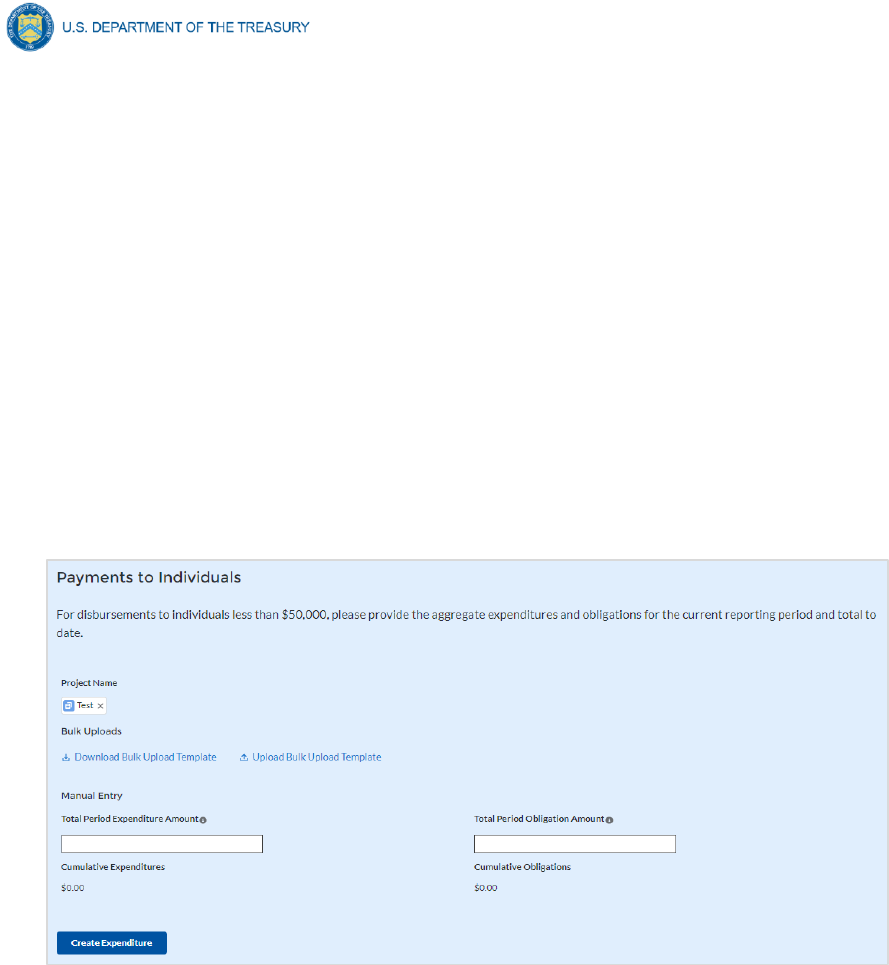

3. Payments to Individuals

For disbursements to individuals less than $50,000, recipients should complete the “Payments

to Individuals” box (see Figure 45) with expenditure information. Once this information has been

entered, click the Create Expenditure button on the bottom left of the box.

Figure 45 Payments to Individuals

Alternatively, the Payments to Individuals bulk upload template (Figure 45) may be used and

uploaded with the relevant information. Note the need to manually identify the Project Name as

no Subaward is necessary for Payments to Individuals less than $50,000.

Once entries are complete, click the Next button on the bottom right of the page. This will bring

recipients to the Report tab.

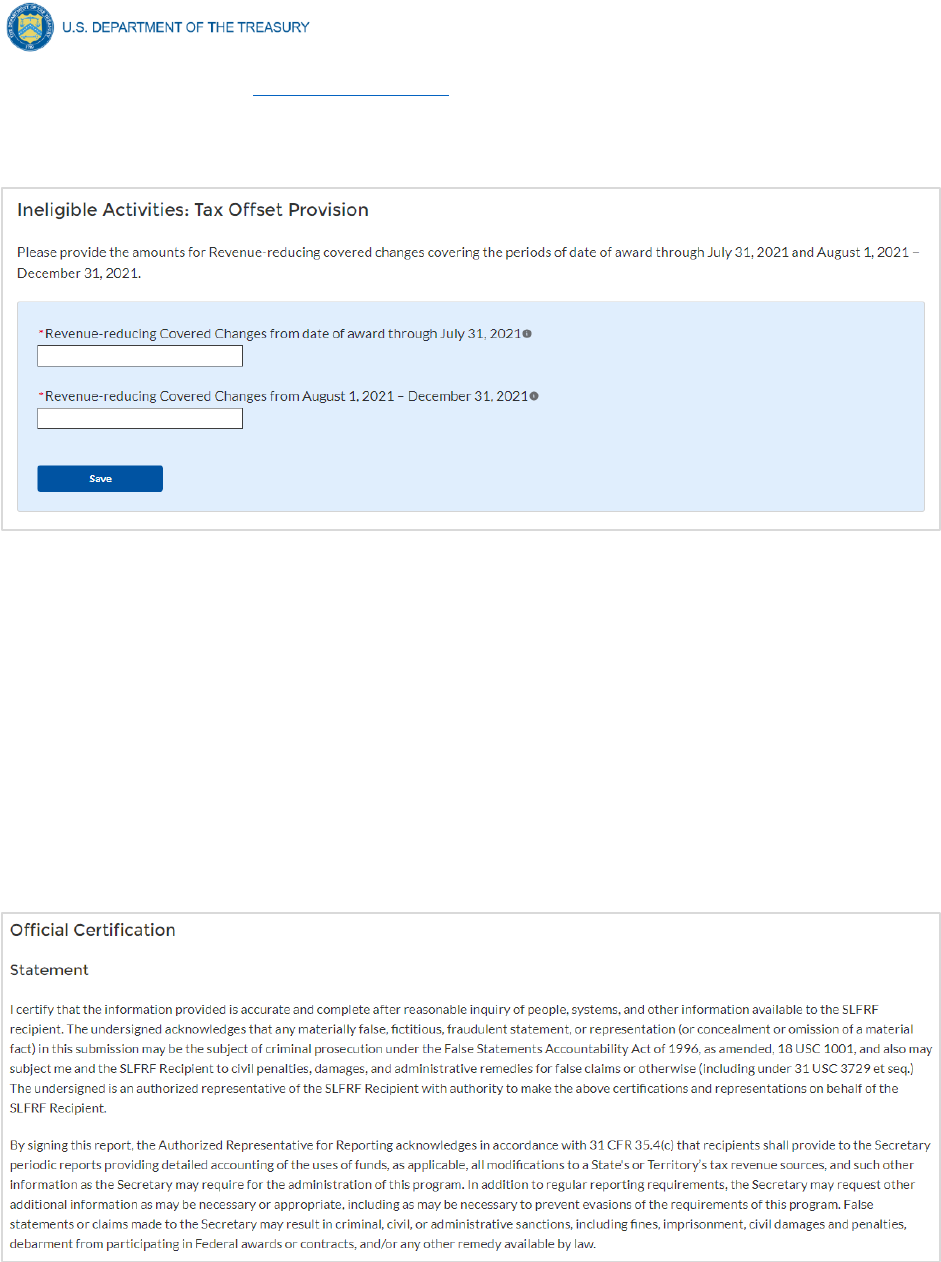

i) Tax Offset Provision (Only for States and U.S. Territories)

Baseline revenue or revenue-increasing covered charges information are not required at this

time. State and U.S territory recipients should provide the amount of revenue-reducing covered

changes covering the periods of date of award through July 31, 2021 and separately, August 1,

2021 through December 31, 2021. (See Figure 46).

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 39

See Section C (11) of the Reporting Guidance for additional information.

Additional guidance will be forthcoming for additional reporting requirements regarding the tax

offset provision.

Figure 46 Tax Offset Provision Screen

j) Official Certification

On this screen, the Authorized Representative for Reporting (ARR) will be asked to certify

information pertaining to the Project and Expenditure. By certifying this submission, the ARR is

confirming that all reported information is accurate and approved for submission (see Figures 47

and 48).

Users who are not designated as an ARR will not be presented with the screen.

1. The ARR’s Name, Title, Telephone Number, and E-Mail Address will be presented on

screen for review.

2. Allow the Certifying Official to review all prior screens and entries to verify accuracy of

the inputted record.

Figure 47 Official Certification

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 40

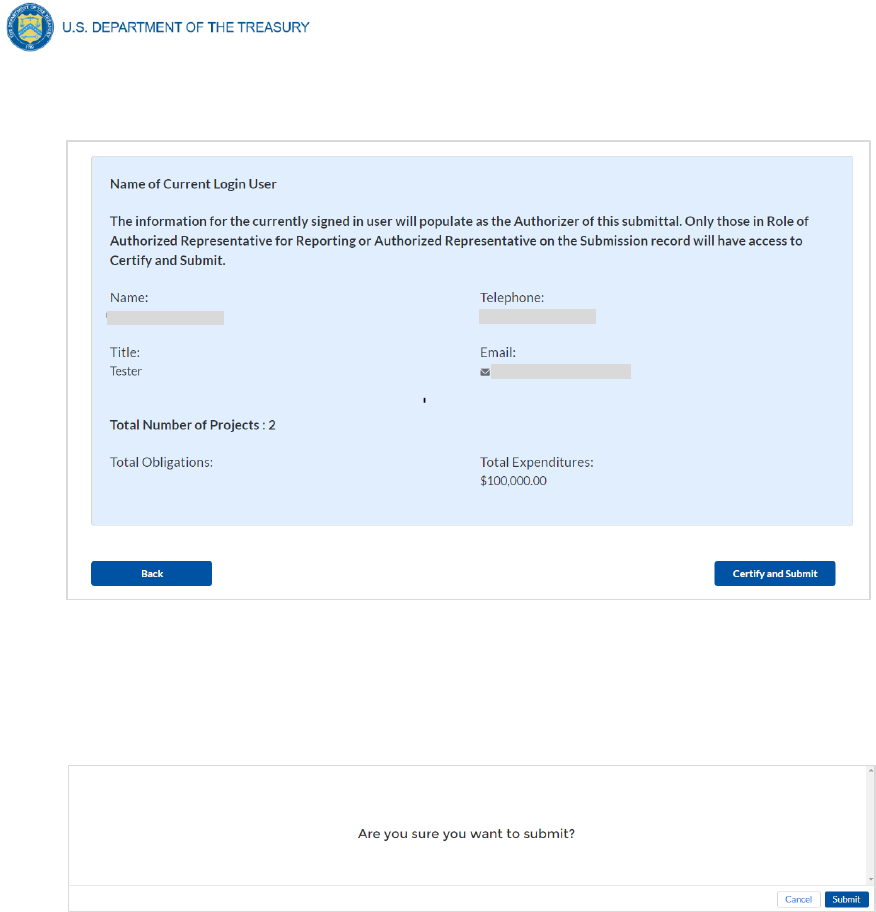

3. Verify information included in Figure 48 and confirm that the values presented are as

expected based on the information included or uploaded in previous screens.

Figure 48 Summary of Reported Information

4. When certifying and submitting the report, a confirmation box will appear asking if the

recipient is sure it wants to submit (see Figure 49).

Figure 49 Submission Verification

Coronavirus State and Local Fiscal Recovery Funds:

Project and Expenditures Report User Guide 41

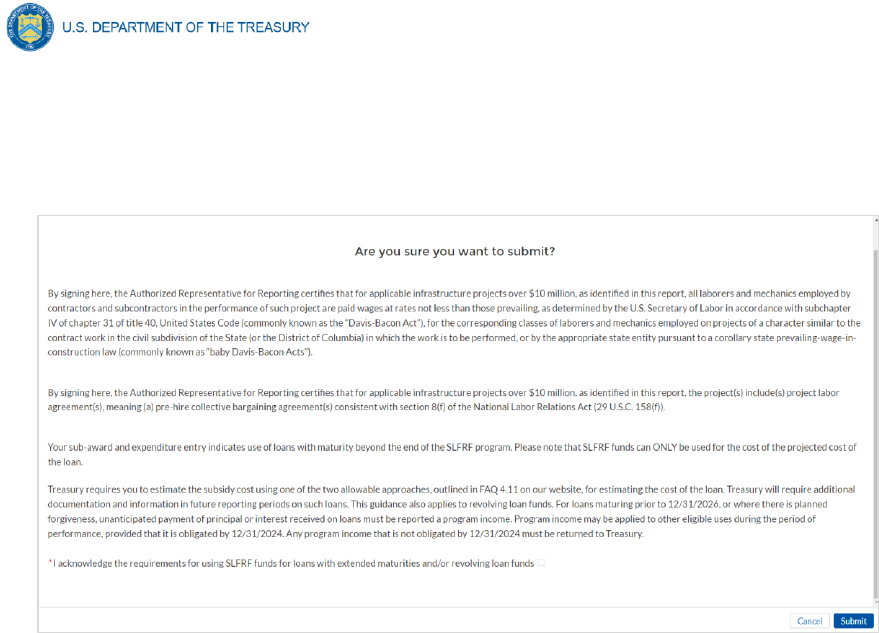

5. A confirmation box may also appear with additional certification language depending on

the programmatic data inputs in the user’s report. Figure 50 shows an example of

project-dependent certification language.

Figure 50 Submission Verification with additional language